Publicly traded companies are all buying cryptocurrency assets, but who is actually making money?

Who didn't make money? Answer: A new investor.

Original Article Title: Facts vs. Myths: The Truth About Crypto Treasury Companies

Original Article Author: Jeff Dorman, CFA

Original Article Translation: TechFlow

Crypto Treasury Companies: Facts vs. Myths

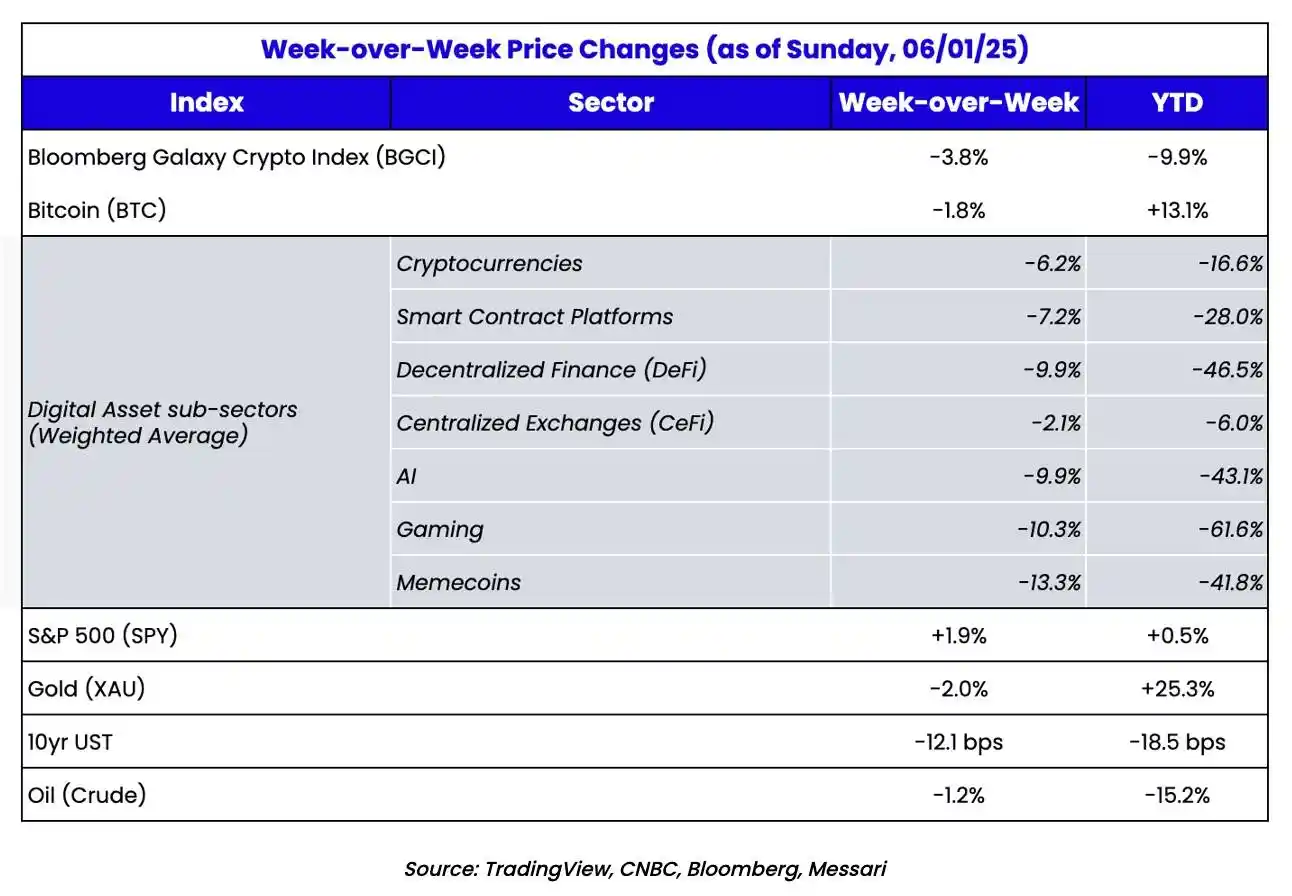

After six consecutive weeks of gains, the Bloomberg Galaxy Crypto Index (BGCI) finally saw a pullback last week, while stocks and US Treasuries both rose. Despite the ongoing discussion about the "breaking" of the US Treasury market, it is worth noting that over the past two years, the US 10-year Treasury yield has actually fluctuated within a 100 basis point range, yet another example of a narrative-driven fact.

When it comes to narratives, the increasing number of US publicly traded companies purchasing Bitcoin and other digital assets has undoubtedly become a market hot topic. However, as usual, this trend is also accompanied by many misunderstandings. Therefore, we will do our best to clarify the facts and misconceptions behind these new digital asset buyers.

Some refer to these companies as "Bitcoin Treasury Companies," while others call them DATs (Digital Asset Treasury Companies). Regardless of the terminology used, these companies are essentially new shell companies designed to hold digital assets. This is different from the original Bitcoin Treasury Companies. Over the past five years or more, we have been discussing the phenomenon of some publicly listed companies incorporating Bitcoin into their balance sheets for various reasons.

These companies can be categorized into several types:

Some are regular companies that experimentally hold Bitcoin, such as Tesla and Block (formerly Square);

Some are crypto-native companies, such as Coinbase and Galaxy, which naturally hold these assets through their core businesses;

And some are Bitcoin mining companies, whose core business is to hold Bitcoin.

The growth of Bitcoin on these companies' balance sheets is easily trackable and sometimes even drives stock price increases. However, in most cases, the amount of Bitcoin held does not overshadow their core business. Additionally, until recently, the Financial Accounting Standards Board's (FASB) accounting standards regarding holding Bitcoin posed a significant EPS downside risk compared to upside gains.

Conversely, these companies' impact on Bitcoin's price is usually limited because they often do not make large-scale Bitcoin purchases through the open market. Most companies simply accumulate Bitcoin through their day-to-day operations, and for those that do buy Bitcoin, the amounts are relatively small.

Source: BitcoinTreasuries.net

Meanwhile, MicroStrategy (stock ticker: MSTR) has gradually become the first truly "Bitcoin company," with its sole focus as a publicly traded company being to acquire Bitcoin. Five years ago, we first took notice of MSTR when it announced its initial Bitcoin purchase plan, causing its stock price to instantly surge by 20% and attracting widespread market attention. As we wrote back in August 2020:

"MSTR's stock price surged by 20% in the week following the announcement, likely resulting in a busy weekend for junior members of corporate finance departments worldwide as they feverishly researched Bitcoin. Remember 2017? Companies would go out of their way to mention 'blockchain' on earnings conference calls, despite having no clue how to actually use blockchain or any concrete plans, merely because the market rewarded companies that appeared to be on the cutting edge of technology? Well, get ready for Bitcoin's replay."

MSTR's initial Bitcoin purchases were made with cash from its balance sheet, but over the past five years, its true "genius" has been in how effortlessly and frequently it taps into the capital markets. While MSTR still has a core business—generating $50-150 million in annual EBITDA through business intelligence and enterprise software analytics services—that business has quickly been overshadowed by its Bitcoin purchasing behavior.

Unlike other public companies attempting to emulate it, MSTR's existing cash flows come from its subsidiary (formerly core) business lines, which can be used to cover corporate expenses and debt service. This distinction sets it significantly apart from other public companies.

Source: ChatGPT and MicroStrategy Financial Reports

By leveraging debt, convertible debt, preferred stock, and the equity markets for new rounds of financing to purchase Bitcoin, MSTR has opened the door for an entirely new cohort of investors to access crypto asset investment opportunities previously out of reach.

Although I'm too lazy to delve into the specifics of each funding round (these details are not crucial to my point anyway, as this content is generated through ChatGPT), MSTR's "magic" in the capital markets is indeed impressive: over the past five years, it has demonstrated the sheer elegance of how the capital markets operate.

Source: ChatGPT

Each new round of funding and Bitcoin purchase has further driven up the price of Bitcoin (BTC) due to its transaction size and signaling effect for future purchases. Simultaneously, this has also propelled the rise of MicroStrategy's (MSTR) stock price as the market starts to pay attention to new metrics such as "per-share Bitcoin" and "Bitcoin yield" that didn't exist before. Essentially, the sole objective of this "company" MicroStrategy has shifted to increasing its Bitcoin reserves, benefiting all participants in the process.

Holders of convertible bonds and preferred stock are actually playing a game of "cheap volatility," capitalizing on the volatility of MSTR's stock and Bitcoin prices. Meanwhile, direct debt holders are only concerned with the fixed income return, which is easily supported by the EBITDA that MSTR can still generate through its old core business. At the same time, equity investors profit from the premium on MSTR's stock, which is far above its Bitcoin net asset value (NAV) on the balance sheet.

Everyone is a winner! Of course, when everyone is winning, two things usually happen:

The Critics' Voices Grow Louder

Critics have started angrily posting on the internet, attempting to find ways to question the feasibility of this strategy. We first responded to these absurd allegations as early as 2021. At that time, many market participants firmly believed that MSTR would be forced to sell Bitcoin, completely misunderstanding how the debt covenants operate, not to mention confusing direct Bitcoin ownership with holding leveraged futures positions with marked-to-market prices.

Even today, we still often need to address claims about MSTR posing a systemic risk to Bitcoin, although we have mostly given up on combating this endless debate. We wish Jim Chanos good luck in his recent "long Bitcoin, short MSTR" trade (although based on the reasons we have listed here, this strategy is unlikely to succeed). "Shorting MSTR" has become the new "shorting Tether," a tantalizing trade that appears low-risk high-reward but is actually unlikely to succeed.

The Rise of Imitators

Welcome to the wild new era of the crypto world. Let's delve further into this phenomenon.

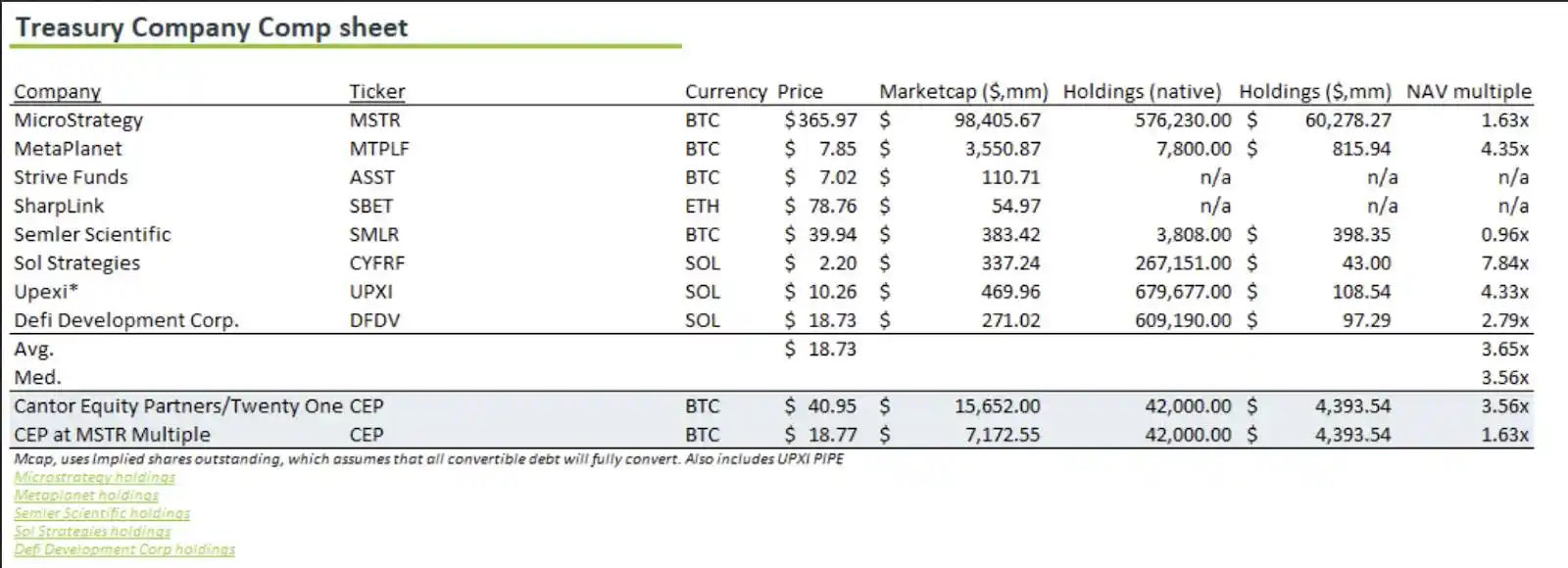

Source: Bloomberg and Arca Internal Calculations

If 2024 was the year of the "Crypto ETF," then 2025 is shaping up to be the year of "SPACs and Reverse Mergers." We once described crypto ETFs as "two steps forward, one step back":

"Many view ETFs as a win for real-time settlement assets, but in reality, a Bitcoin ETF is actually shoving a real-time settlement system (blockchain) into an outdated T+1 settlement product (ETF). Isn't that a step backward? As an industry, we should strive to bring global assets onto the blockchain rather than force on-chain assets into Wall Street's archaic systems."

While we acknowledge this as a necessary step to drive adoption and interest, the viewpoint still holds. There is a significant difference between "blockchain technology" and "crypto assets." Our focus is more on bringing the world's most popular assets (such as stocks, bonds, real estate) onto the blockchain rather than cramming low-quality crypto assets into outdated systems. However, the trend of fitting crypto assets into stock shells is not slowing down. Let's see what's currently unfolding.

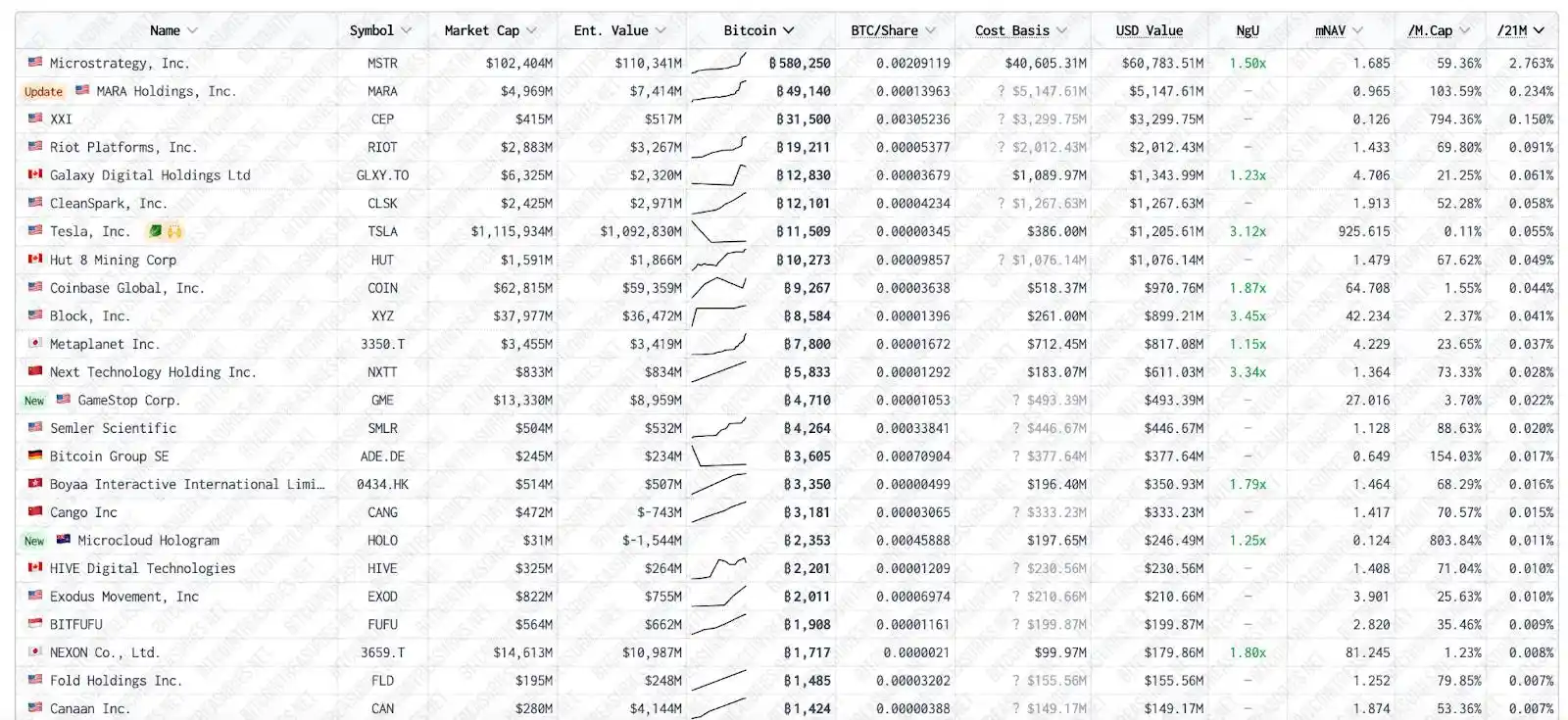

Special Purpose Acquisition Companies (SPACs) and reverse mergers have been around for a while, but rarely utilized for a singular purpose adoption. Yet, that is precisely the current scenario. If you have a publicly traded shell, it can be used to acquire crypto assets, aiming to trade at a significant premium to Net Asset Value (NAV). These new structures often differ slightly from MicroStrategy. Some companies hold solely Bitcoin, attempting to mirror MSTR's playbook entirely (despite lacking the brand recognition and capital markets expertise of MSTR); while others have acquired new assets—some holding Ethereum (ETH), some holding Solana (SOL), some holding TAO, with more emerging assets. Arca currently receives 3 to 5 new pitches per week from investment banks.

Here are some recent transaction examples that have been announced and are in the process of fundraising (may not be exhaustive):

SharpLink Gaming (SBET)

· Recent Activity: May 2025

· Funding Method: $4.25 Billion Private Investment in Public Equity (PIPE)

· Acquisition of Crypto Asset: Ethereum (ETH)

Trump Media & Technology Group (DJT)

· Recent Activity: May 2025

· Funding Method: Raised $2.3 Billion through Stock and Convertible Bond Sales

· Acquisition of Crypto Asset: Bitcoin (BTC)

GameStop Corp. (GME)

· Recent Activity: May 2025

· Funding Method: $1.5 Billion Convertible Bond Offering

· Acquisition of Crypto Asset: 4,710 BTC

Jetking Infotrain (India)

· Recent Activity: May 2025

· Funding Method: Raised ₹6.1 Million through Equity Sale

· Acquisition of Crypto Asset: Bitcoin (BTC)

Meliuz (CASH3.SA - Brazil)

· Recent Activity: May 2025

· Funding Method: Raised 1.5 Billion Brazilian Reais through Stock Offering

· Acquisition of Crypto Asset: Bitcoin (BTC)

· Details: Brazilian fintech company Meliuz announced its initial public offering to raise 1.5 Billion Brazilian Reais (approximately $264.5 million) for the acquisition of Bitcoin. The company plans to issue 17,006,803 common shares as an initial batch.

Sol Strategies Inc. (CSE: HODL, OTCQX: CYFRF)

· Initial Investment: January 2025

· Funding Method:

o $25 Million CAD Unsecured Revolving Credit Facility provided by Chairman Antanas Guoga;

o $27.5 Million CAD (approximately $20 million USD) Convertible Bond provided by ParaFi Capital;

Up to $500 million in convertible bond capacity from ATW Partners, with the first $20 million completed in May 2025.

· Acquired Cryptocurrency: Solana (SOL)

Cantor Equity Partners / Twenty One Capital (CEP)

· Recent Activity: May 2025

· Funding Method: Added $100 million to its crypto business Twenty One Capital, bringing the total funding amount to $685 million. At the same time, existing shareholders (including Tether, Bitfinex, and SoftBank) committed Bitcoin in physical form through the existing equity structure.

· Acquired Cryptocurrency: Bitcoin (BTC)

Upexi Inc.

· Recent Activity: April 2025

· Funding Method: Raised $100 million to establish a Solana reserve

· Acquired Cryptocurrency: Solana (SOL)

· Details: Purchased SOL through a $100 million PIPE (Private Investment in Public Equity) and plans to further increase the "Sol-per-share" through equity and debt issuance.

DeFi Development Corp (formerly Janover)

· Recent Activity: April 2025

· Funding Method: Raised $42 million to establish a Solana reserve fund and plans to raise an additional $1 billion

· Acquired Cryptocurrency: Solana (SOL)

These cases illustrate that more and more publicly traded companies are incorporating cryptocurrency assets into their financial strategies, usually funding these acquisitions through debt or equity offerings. However, who is making money from these transactions?

Investment Bank

Investment banks earn fees by underwriting PIPEs or conducting reverse mergers, a strategy that carries almost no risk, allowing them to profit regardless of the transaction outcome. As a result, they will not cease facilitating such deals.

Shell Company Owners/Management

Assuming $100 million is raised through a new PIPE issuance, with $85 million used to purchase cryptocurrency assets and the remaining $15 million used for "operating expenses." These "operating expenses" include higher salaries—a handsome income for the management team.

Stockholders Prior to Reverse Merger or SPAC Announcement

Most of these shell companies typically had a market capitalization of less than $20 million before being transformed into crypto stock shells. Some of the investors holding these stocks may have had advance knowledge through insider information that the stock would be transformed into a crypto company, while others were purely lucky. However, undoubtedly, the real profits came from these stocks skyrocketing 500%-1000% or even more after the announcement.

Who Didn't Make Money? — New Investors.

Unlike MicroStrategy, we already have 5 years of historical data proving that its debt, convertible debt, preferred shares, and equity holders have all been able to profit. However, for these new investors in these new types of transactions (those providing funds for PIPE or SPAC), there is currently no evidence indicating they will make money. These transactions are relatively new, and most private investors have not yet converted their private shares into public shares (usually requiring at least 90 days). Therefore, these transactions are still ongoing, and investors are still buying in.

If these stocks continue to trade at a significant premium to Net Asset Value (NAV) after the new investor unlocks, we will see more similar transactions emerge. But if these stocks start to plummet, even falling below NAV, then the game is over. It might take a few more months for us to know how the market will react when these shares unlock.

However, there is currently a misconception spreading in the market: these unlocks pose a risk to the shell company equity investors rather than to the underlying crypto assets they hold. Unless financed by debt and unable to pay interest (i.e., default), there is almost no mechanism that would force the sale of the underlying crypto assets. Additionally, these new shell companies are currently small and cannot access the debt markets. This type of operation is currently limited to MicroStrategy (MSTR) and a few other large players.

For equity and preferred stockholders, they do not have the right to demand the sale of underlying assets unless the stock price is far below Net Asset Value (NAV) to the point where some aggressive investor starts buying up shares in large quantities and attempts to take over the board to sell the underlying crypto assets to buy back stock. This scenario may happen in the future, but it is not a significant risk today. Once such an event occurs, most stocks will quickly narrow the gap with NAV as the market realizes this pattern can be exploited repeatedly.

This situation is very similar to the status of the Grayscale Trust Fund before the ETF launch. At that time, there was no risk of forced selling of its underlying crypto assets by Grayscale... The real risk was that the trust fund (stock) was trading at a price below its Net Asset Value (NAV). Eventually, this did happen, causing harm to equity investors but having no impact on crypto asset holders.

Today, every crypto risk investor holding a large amount of high-inflation, low-demand junk tokens is discussing how to squeeze these tokens into an equity shell company. However, this will not automatically create demand, just like most newly launched ETFs have failed to attract investors. Creating an investment tool and generating demand are two different things. Although these investment tools will continue to be created, it is still uncertain at the moment whether these stocks will truly attract market demand.

Is there a possibility that these shell companies can maintain a long-term premium above NAV? The answer is possibly, but the conditions are stringent. Perhaps one day, MicroStrategy (MSTR) will become the "Berkshire Hathaway" of the crypto space. By then, Bitcoin may become an extremely scarce and highly sought-after asset, to the point where companies are willing to accept a lower acquisition offer from Michael Saylor simply because he can pay with precious Bitcoin.

Another possible way to sustain the premium of shell companies is for these companies to become more creative in selecting underlying assets. For example, they can hold high-quality tokens such as HYPE that are currently not listed on any centralized exchange, thus providing an opportunity for a new group of investors to access HYPE. This scarcity and uniqueness may attract investors willing to pay a premium. However, these scenarios are all long-term possibilities.

Nevertheless, like ETFs, some shell companies will succeed, and some will not. But if bankers want to keep the "profit train" moving forward, they must start to become more creative. If simply stuffing crypto assets into an equity shell company, then there must be continuous innovation within the shell company — making it valuable and difficult to obtain through other means.

However, I believe that these equity shell companies will not have a negative impact on crypto assets themselves, at least not in the short term. Without debt in the capital structure, there is no forced selling mechanism. And, I think we may still be long trying to dispel misunderstandings about these shell companies, just as we have done on many crypto topics.

Tokens Can Still Serve as a Tool for Capital Formation

The recent trend from token financing to equity financing for shell companies can be seen as "two steps forward, one step back." However, this does not mean that token sales have stopped; it's just that the related discussions have decreased.

We often say: "Tokens are the greatest capital formation and user acquisition mechanism in history, capable of aligning all stakeholders, creating lifelong brand advocates and core users." The idea is simple: instead of issuing equity or debt where investors cannot become product users and customers cannot benefit from the company's growth, why not directly issue tokens to customers, thus aligning all stakeholders in one go? This is exactly what the ICOs (Initial Coin Offerings) attempted in 2017 until US regulators called a halt.

The good news is that regulatory pressure is easing, allowing some token financing to make a comeback. The bad news is that currently, most token financing is still limited to the "pure crypto" realm—meaning those crypto and blockchain-native companies that would not exist without blockchain technology. The missing piece is a world where non-crypto-native companies (such as regular gyms, restaurants, and small businesses) can also start issuing tokens to fund their operations and align stakeholders' interests.

The "Internet Capital Markets" is a term used to describe this emerging theme. This idea is not new (in fact, we've been writing about it for seven years—I first wrote about crypto in a blog post involving this concept, back when Arca didn't even have a website). But now, this idea is finally starting to gain some traction.

Launchcoin is one of the key platforms driving the next generation of token issuance. Launchcoin (which has its own token) supports Believe, a token issuance platform that is leading the "Internet Capital Markets" narrative. On the Believe platform, tokens make their debut through bonding curves and then enter the Meteora platform to enhance liquidity. This platform is attractive because many trusted Web2 companies have tokenized (created tokens) through Believe. While direct token value accrual has not yet been achieved, the potential is vast, making Launchcoin a pioneering force in this narrative.

In other words, Launchcoin and Believe are working towards a vision where every city government, university, small business owner, sports team, and celebrity can issue their own tokens. We have seen many examples showing that tokens can be used to shore up a company's balance sheet or for restructuring. For example, Bitfinex with its LEO token and Thorchain with its debt token have successfully raised funds. This type of token financing model is what makes the crypto industry exciting, as opposed to just being equity shell companies.

Currently, both models coexist, and understanding the difference is crucial.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

$3.21B in Bitcoin Options and $624M in Ethereum Options Expire on June 6

Aave (AAVE) Approaches Key Resistance – Is a Bullish Breakout on Horizon?

The Best Crypto Projects to Join in June 2025: Dogecoin, Shiba Inu, Bonk & BlockDAG Lead The Market!

Discover the best crypto projects of June, featuring Dogecoin, Shiba Inu, Bonk, and BlockDAG. Each of these coins has something unique to offer, so explore their potential and what's next for 2025.1. BlockDAG: The Only Altcoin with 2678% ROI Potential!2. Dogecoin’s Next Move: Can it Break $0.25?3. Shiba Inu: Strong Community, But June’s a Challenge4. Bonk: A Meme Coin with Real UtilityFinal Thoughts

Top Cryptos to Buy in June 2025 for Explosive Growth: Arctic Pablo, FLOKI, Memecoin