Wall Street continues to sell off—how much further will bitcoin fall?

The first week of November saw very poor sentiment in the crypto space.

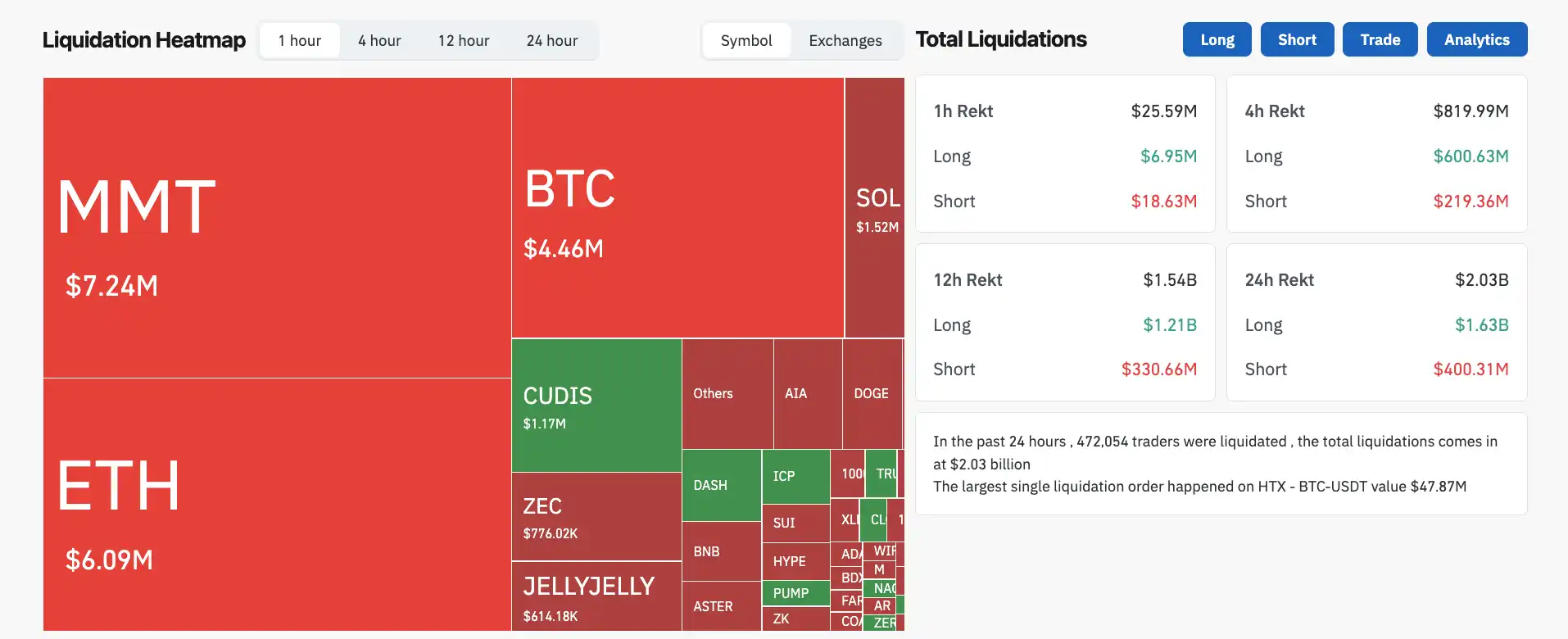

Bitcoin has already dropped to a new low below the "10.11" crash, failing to hold the $100,000 mark and even falling below $99,000, marking a new six-month low. Ethereum touched as low as $3,000.

The total amount liquidated across the network in 24 hours exceeded $2 billion, with longs losing $1.63 billion and shorts liquidated for $400 million.

Data source: CoinGlass

The worst was a BTC-USDT long position on the HTX exchange, which was liquidated for $47.87 million in a single order, topping the network-wide liquidation leaderboard.

There are always some reasons behind a drop, which we can analyze in hindsight.

Within the Industry

For two consecutive days, projects have run into trouble. On November 3, the long-established and well-known DeFi project Balancer was hacked for $116 million due to a code issue. Balancer is DeFi infrastructure, even older than Uniswap, so such a code problem is a huge blow to the industry.

On November 4, a wealth management platform called Stream Finance collapsed, with the official statement claiming a loss of $93 million. The problem is that it’s unclear how the loss occurred, and the official team hasn’t explained; the community speculates it happened on the day of the "10.11" crash.

There’s only so much money in the crypto space, and another $200 million disappeared in the past two days.

From a Macro Perspective

Looking at global capital markets, November 4 saw declines worldwide—Japanese and Korean stocks at new highs also fell, and US stocks were down in pre-market trading.

First, regarding interest rate cuts: last Wednesday, the Federal Reserve spoke, and the certainty of a December rate cut seemed to decrease again, suggesting there is no rush to cut rates.

Then, ETFs also saw net outflows. Last week, US-listed bitcoin ETFs had a net outflow of $802 million, and on Monday, November 3, another $180 million flowed out.

On November 5, another event: the US Supreme Court will hold oral arguments in the "tariff trial," reviewing the legality of Trump’s global tariffs. The uncertainty lies in that if the final ruling goes against Trump, tariffs may be canceled, leading to new policy adjustments.

The US federal government "shutdown" has entered its 35th day, tying the longest shutdown in US history. The government closure has led institutions to hedge high-risk assets, triggering sell-offs. This may be one of the core reasons for the recent sharp decline.

According to a previous article by Wallstreetcn, analysis shows that the shutdown forced the US Treasury to sharply increase its general account (TGA) balance at the Federal Reserve from about $30 billion to over $100 billion in the past three months, a five-year high. This process effectively drained over $70 billion in cash from the market.

This large-scale liquidity drain has a tightening effect comparable to several rate hikes. Key financing rate indicators are under pressure across the board. According to Bloomberg, the Secured Overnight Financing Rate (SOFR) surged by 22 basis points on October 31 (UTC+8), far above the Fed’s target range, indicating that actual market financing costs have not fallen with the Fed’s rate cuts. Meanwhile, usage of the Fed’s Standing Repo Facility (SRF) is also approaching historical highs.

Spot ETFs Continue to Bleed

The ETF outflows are actually more severe than imagined.

From October 29 to November 3, IBIT, the world’s largest bitcoin spot ETF under BlackRock, which holds a 45% market share, saw a cumulative net outflow of $715 million over four trading days, accounting for more than half of the $1.34 billion total outflow in the US bitcoin ETF market.

Looking at the whole week, from October 28 to November 3, IBIT had a net outflow of $403 million, accounting for 50.4% of the market’s $799 million outflow. On October 31 alone (UTC+8), it saw a single-day outflow of $149 million, setting an industry record for the highest single-day outflow.

On November 4, BlackRock’s Coinbase Prime custody address also made on-chain adjustments of 2,043 BTC and 22,681 ETH, leading the market to speculate that ETF holders are still continuously selling crypto assets.

Although IBIT’s assets under management still remain between $9.5 billion and $10 billion, holding about 800,000 bitcoin (3.8% of the circulating supply), the four-day outflow corresponds to about 5,800 BTC, accounting for 0.7% of its holdings.

Although the proportion is not large, as the industry leader, the demonstration effect is significant.

Looking at the other major bitcoin spot ETFs, the top five are BlackRock’s IBIT, Fidelity’s FBTC, Grayscale’s GBTC, Bitwise’s BITB, and ARK’s ARKB in partnership with 21Shares.

Fidelity’s FBTC had a net outflow of $180 million during the same period, accounting for 0.7% of its size, which is relatively mild; Grayscale’s GBTC saw outflows slow after its fee reduction, with $97 million outflow this week; the smaller BITB and ARKB saw weekly changes of around $50 million each.

This wave of redemptions is essentially due to a sharp drop in investor risk appetite, in sync with macro high interest rate expectations and bitcoin’s technical breakdown.

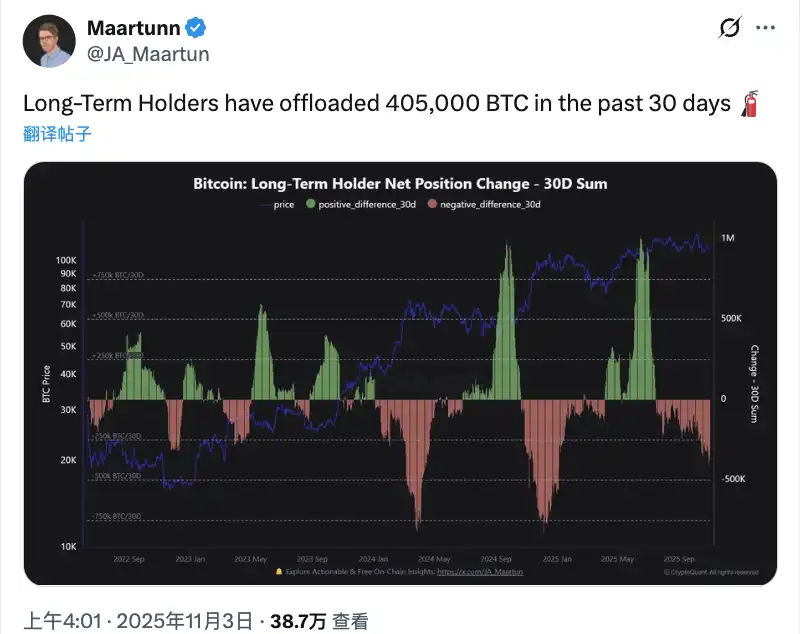

Long-term On-chain Holders Are Also Cashing Out Aggressively

Even more aggressive than ETFs are the old players on-chain.

In the past 30 days (October 5 to November 4), wallet addresses holding coins for more than 155 days, known as "long-term holders" (LTH), have cumulatively sold about 405,000 BTC, accounting for 2% of the circulating supply. At an average price of $105,000 during the period, they cashed out over $42 billion.

This group still holds about 14.4 to 14.6 million BTC, accounting for 74% of the circulating supply, and remains the largest supplier in the market. The problem is that their selling pace has matched the price trend exactly: after bitcoin hit a record high of $126,000 on October 6, profit-taking accelerated significantly; on the day of the "10.11" flash crash, 52,000 BTC flowed out in a single day (UTC+8); from late October to early November, combined with four consecutive days of ETF net outflows, daily sales exceeded 18,000 BTC.

On-chain data shows that the main sellers are "mid-generation" wallets holding 10 to 1,000 BTC—those who bought 6 months to a year ago and now have about 150% paper profits. Whales holding over 1,000 BTC are actually slightly increasing their holdings, indicating that top players are not bearish, and it’s mainly medium-sized profit-takers cashing out.

Historically, in March 2024, LTHs sold 5.05% in a single month, and bitcoin fell 16%; in December last year, they sold 5.2%, and the price dropped 21%. This time, October’s sell-off was 2.2%, with only a 4% drop, which is actually mild.

But with both ETFs and on-chain holders bleeding at the same time, the combined forces are too much for the market to withstand.

Assessing the Bottom of the Decline

glassnode published a market view stating that the market continues to struggle above the short-term cost basis (around $113,000), which is the key battleground for bulls and bears. If it fails to regain this level, it may further fall to the actual price for active investors (around $88,000).

CryptoQuant CEO Ki Young Ju posted a series of on-chain data last night, stating that the average cost of bitcoin wallets is $55,900, meaning holders are on average up about 93%. On-chain capital inflows remain strong. The price cannot rise due to weak demand.

10x Research CEO Markus Thielen said after the market drop that bitcoin is approaching the support line since the October 10 crash. If it falls below $107,000 (UTC+8), it may test $100,000 (UTC+8).

Chinese crypto KOL Banmuxia publicly stated today, "The traditional 4-year bull cycle has ended. Bitcoin will gradually fall to $84,000 (UTC+8), then experience several months of complex consolidation, and by the end of next year or early the following year, will follow the US stock bubble up to $240,000 (UTC+8)."

At present, the only good news seems to be that, historically, bitcoin has averaged gains in November.