DTCC News Sparks Speculation on Bitcoin ETF Inflow Reversal

👇1-11) The Deposit Trust Company (DTCC) has just announced that come April 30, ‘no collateral value will be given for any ETF or other investment vehicle that includes Bitcoin or any other cryptocurrency as an underlying investment, hence will be subject to a 100% haircut.’

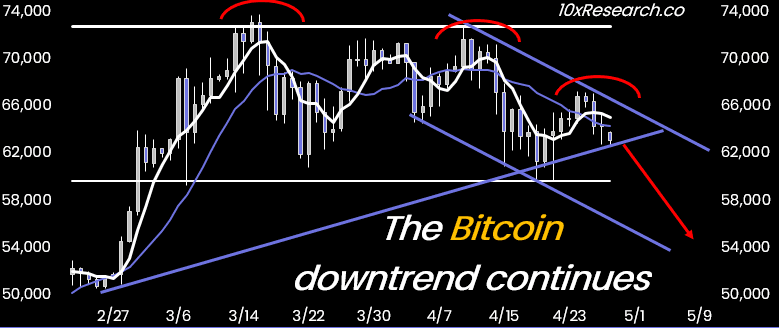

👇2-11) As we have pointed out, Bitcoin is making lower highs—a new downtrend seems to be in place (see chart below). This is where the DTCC statement could be impactful. We wrote about the Self-Reinforcing Bitcoin Mechanism At Play Framework on April 4, and there is a risk that inflows could, to some extent, reverse.

Bitcoin technical analysis

👇3-11) This could be a big deal for Bitcoin ETFs as the DTCC provides clearing and settlement services for the financial markets in America.

👇4-11) While only a few people know the DTCC, the entity became famous late last year when it suddenly started listing Bitcoin ETFs from various issuers months before the SEC’s approval. This caused Bitcoin prices to rally as the probability of regulatory approval increased.

But why should you care?

The ETFs are already approved. Well, here is why:

👇5-11) A few weeks ago, we claimed that the ETF inflows would likely stop as crypto trading volumes and the funding rate shrank significantly. A lower funding rate would predict fewer ETF inflows as we estimated that a large part of the outright Bitcoin ETF buying came from arbitrage-seeking hedge funds that sold CME Bitcoin futures against their IBIT Blackrock Bitcoin ETF holdings.

👇6-11) The key here is how this trade might have gotten financed, as shorting CME Bitcoin futures generally requires a vast collateral position, making this long ETF short futures trade less capital efficient.

👇7-11) This is where collateral management comes in. Large institutions could get margin release when they post both legs (long and short) to the same prime broker, for example, with the DTCC potentially signing off on assigning the collateral amount. If Bitcoin ETFs no longer qualify for margin release, we could see this arb trade removed, and ETFs could see more pronounced outflows.

Bitcoin CME Shorts by Trader Category

👇8-11) For example, CME Bitcoin Futures shorts by hedge funds increased from $2.5bn by the end of January to $6.9bn in early April and has remained relatively flat at $6.3bn. ‘Coincidently, since early April, ETF inflows have been $-40m – they stopped – coinciding when the CME Futures premium crushed down near zero.

👇9-11) The DTCC news is certainly not bullish for TradeFi investors to put on more Bitcoin exposure. As mentioned, traders should monitor the roll spread between various CME Bitcoin calendar futures.

👇10-11) As the CME Bitcoin futures premium compressed, the arb trade (long Bitcoin ETF vs. short Bitcoin futures) has become unattractive as the declining trading volumes predicted weeks in advance. If the DTCC news is negative, we should see an impact by next week - when uncertainties are high with the refunding of the US debt announcement and FOMC statement, where Fed Chair Powell could become marginally more hawkish.

👇11-11) As mentioned on Thursday, Bitcoin needed to reclaim the 67,000 ‘high’ for us to brush off the bearish signals of the last few weeks. As Bitcoin has failed to rebound, we continue to expect lower prices. This DTCC news is another negative sign that, at this point, TradeFi is unlikely to channel large amounts of fiat into Bitcoin. Our 52,000/55,000 target remains valid.