Can Bitcoin Fix US Housing? FHFA’s Crypto Mortgage Move Gains Attention as Crisis Deepens

Google searches for “help with mortgage” now exceed 2008 crisis levels, highlighting US housing stress. FHFA’s Bitcoin mortgage recognition marks progress but offers limited real relief.

Google searches for “help with mortgage” have now surged past the peak of the 2008 Global Financial Crisis, signaling mounting stress in the US housing market.

Analysts warn that affordability pressures are deepening, with late rent payments climbing and mortgage costs rising at a pace far outstripping income growth.

Mortgage Rates Signal Shifting Economic Pressures for Crypto Markets

According to housing analyst Nick Gerli, incomes have grown just 21.9% since 2019. Meanwhile, mortgage costs have risen 91.9% in the same period.

“Costs to buy have gone up four times faster than incomes. Not sustainable,” Gerli wrote.

Other commentators, including Darth Powell and Neil, pointed to skyrocketing late rental payments. There is also a growing struggle for homeowners to keep pace with monthly bills.

Late rental payments are skyrocketing

— Darth Powell

Meanwhile, Polymarket and Barchart data show that searches for mortgage help have surpassed 2008 levels. This reflects how financial stress is spreading beyond renters to homeowners.

JUST IN 🚨: Google Searches for "help with mortgage" has now surpassed the peak of the 2008 Global Financial Crisis

— Barchart

With affordability collapsing, home-buying activity remains muted even as credit conditions tighten.

FHFA’s Crypto Experiment Pushes Adoption, But With Strings Attached

Against this backdrop, the Federal Housing Finance Agency (FHFA) attempted to ease access to credit in June by allowing Bitcoin and certain cryptocurrencies to count as assets for mortgage eligibility.

The move applies to applicants through Fannie Mae and Freddie Mac. It marked the first time the federal mortgage system formally recognized crypto in asset assessments.

However, the program had limitations. Only crypto held on US-regulated custodial exchanges qualifies, while Bitcoin in cold storage, multisig setups, or self-custody wallets does not.

Applicants can also not pledge these assets as collateral, as crypto holdings count toward net worth in the assessment process.

Critics argue that the approach undermines Bitcoin’s core principle of self-sovereignty.

“It looks like bitcoin held in self-custody will NOT count as an asset for consideration on home loans. This is a mistake Pulte; self-custody is fundamentally aligned w/American values. It’s trivial to prove ownership of BTC in self-custody,” Nick Neuman.

Bitcoin financial services firm Swan echoed the concern. While Swan acknowledged the move as a win, it recognized the limitations.

Bitcoin does not exist in the eyes of mortgage underwriters unless it is visible on state-regulated custodial platforms.

Bitcoin is being added to the mortgage system.That’s a win—but don’t let it fool you.If your Bitcoin isn’t custodied in a way the state can see, it still “doesn’t exist.”Let’s talk about the real frontier: self-custody in a captured system 🧵👇

— Swan

For Swan, this reflects a larger pattern: first ignoring crypto, then adopting it, but only on terms designed for control.

Notwithstanding, supporters hold that the FHFA’s recognition still marks a breakthrough. By including crypto assets without requiring conversion to US dollars, the agency gave digital assets a foothold in one of America’s most systemically important markets.

For crypto holders, especially those who may be cash-poor but asset-rich, this could open a path to qualifying for mortgages that would otherwise be out of reach.

Still, the housing crisis highlights the limits of crypto’s role. The recognition came just as housing stress surged to levels unseen since 2008, and the narrow scope of eligibility means Bitcoin is unlikely to provide widespread relief.

Instead, crypto’s integration into mortgage credit may remain a niche tool.

On the one hand, it is symbolic of broader financial convergence. On the other hand, it remains far from a solution to the affordability crisis gripping American households.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

UFC Star Khabib Nurmagomedov’s MultiBank Partnership Tokenizes His Global Gym Brand on Mavryk

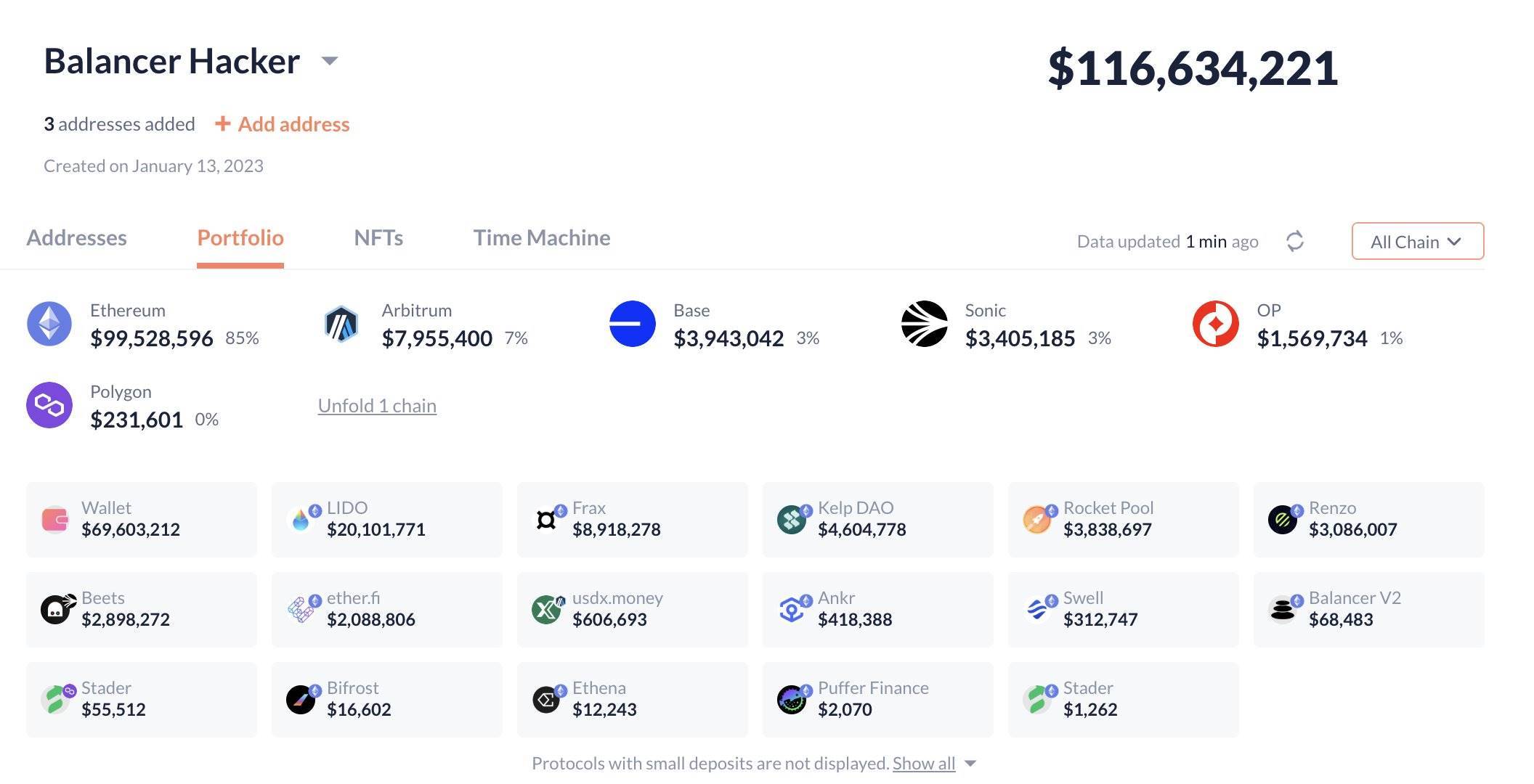

Six incidents in five years with losses exceeding 100 millions: A history of hacker attacks on the veteran DeFi protocol Balancer

For bystanders, DeFi is a novel social experiment; for participants, a DeFi hack is an expensive lesson.

Review of Warplet: How a Small NFT Sparked the Farcaster Craze?

A meme, a mini app, and a few clicks—just like that, the Farcaster community has a brand new shared story.

Hong Kong’s HKMA Launches Fintech 2030 to Drive Future Financial Innovation