Liquidity War 3.0: Bribery Has Become the Market

If you determine the direction of liquidity, you influence who can survive in the next market cycle.

Original Title: Liquidity Wars 3.0 where Bribes Become Markets

Original Author: arndxt, Cryptocurrency Analyst

Translated by: Block Unicorn

I believe we are about to witness another yield war. If you've been in the Decentralized Finance (DeFi) space long enough, you know that Total Value Locked (TVL) is just a vanity metric until it isn't.

In a highly competitive, modularized world of Automated Market Makers (AMMs), perpetual swaps, and lending protocols, what truly matters is who can control liquidity routing. Not who owns the protocol, not even who distributed the most rewards. It's who can convince Liquidity Providers (LPs) to deposit and ensure TVL stickiness. This is where the bribery economy starts.

What used to be informal vote-buying behavior (Curve wars, Convex, etc.) has now been professionalized, evolving into a mature liquidity coordination market equipped with order books, dashboards, incentive routing layers, and in some cases, even gamified participation mechanisms. This has become one of the most strategically important layers in the entire DeFi stack.

Point of Change: From Issuance to Meta-Incentives

In 2021-2022, protocols guided liquidity in a traditional way:

1. Deploy Liquidity Pool

2. Issue Tokens

3. Hope that profit-seeking LPs would stick around even after the APY decreased

But this model is fundamentally flawed—it's passive. Every new protocol is competing with an invisible cost: Opportunity cost of existing capital flows.

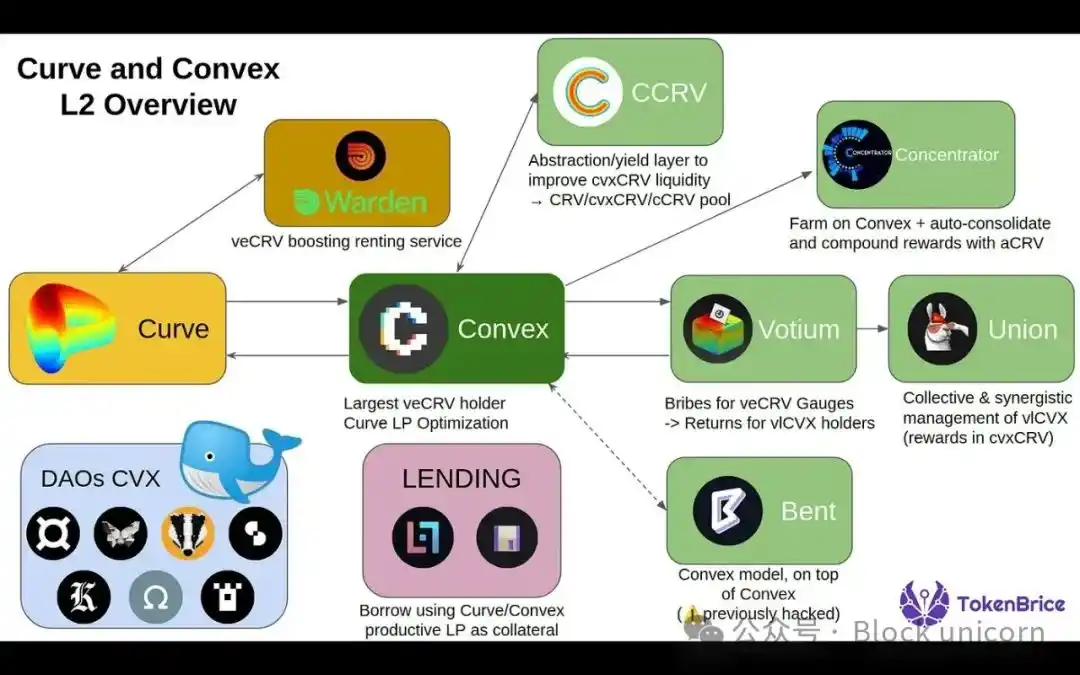

I. Origin of the Yield Wars: Curve and the Rise of the Voting Market

The concept of yield wars started to materialize during the 2021 Curve Wars.

Curve Finance's Unique Design

Curve introduced a voting lockup (ve) tokenomics where users could lock up $CRV (Curve's native token) for up to 4 years to receive veCRV, granting them:

· Curve Liquidity Pool Enhancement Reward

· Governance Power over Voting Weight (which pools can issue)

This creates a metagame around issuance:

· The protocol aims to gain liquidity on Curve.

· The only way to gain liquidity is to attract votes to their pool.

· Therefore, they start bribing veCRV holders to vote in their favor.

Next is Convex Finance

· Convex abstracts the locking of veCRV and aggregates voting power from users.

· It has become the "Kingmaker of Curve," wielding significant influence on the flow of $CRV issuance.

· Projects begin bribing Convex/veCRV holders through platforms like Votium.

Lesson 1: Whoever controls the weight controls the liquidity.

II. Metagame Incentives and Bribery Market

The First Bribe Economy

What initially started as manually affecting issuance has evolved into a mature market where:

· Votium has become an off-chain bribery platform for $CRV issuance.

· Groups like Redacted Cartel, Warden, and Hidden Hand have expanded this to other protocols like Balancer and Frax.

· Protocols no longer just pay issuance fees; they strategically allocate incentive measures to optimize capital efficiency.

Expansion Beyond Curve

· Balancer adopts a vote delegation mechanism through $veBAL.

· Systems like Frax, TokemakXYZ integrate similar systems.

· Platforms like Aura Finance and Llama Airforce further increase complexity in incentive routing, turning issuance into a capital coordination game.

Lesson 2: Rewards are no longer about Annual Percentage Yield (APY) but programmable metagame incentives.

III. Tactics of the Yield War

The following are the protocol's competitive strategies in this metagame:

· Liquidity Aggregation: Aggregating influence through wrappers like Convex (e.g., Balancer's AuraFinance).

· Bribery Campaigns: Reserving a budget for ongoing vote bribes to attract needed issuance.

· Game Theory and Tokenomics: Locking tokens to create long-term alignment (e.g., ve models).

· Community Incentives: Gamifying voting through NFTs, lotteries, or additional airdrops.

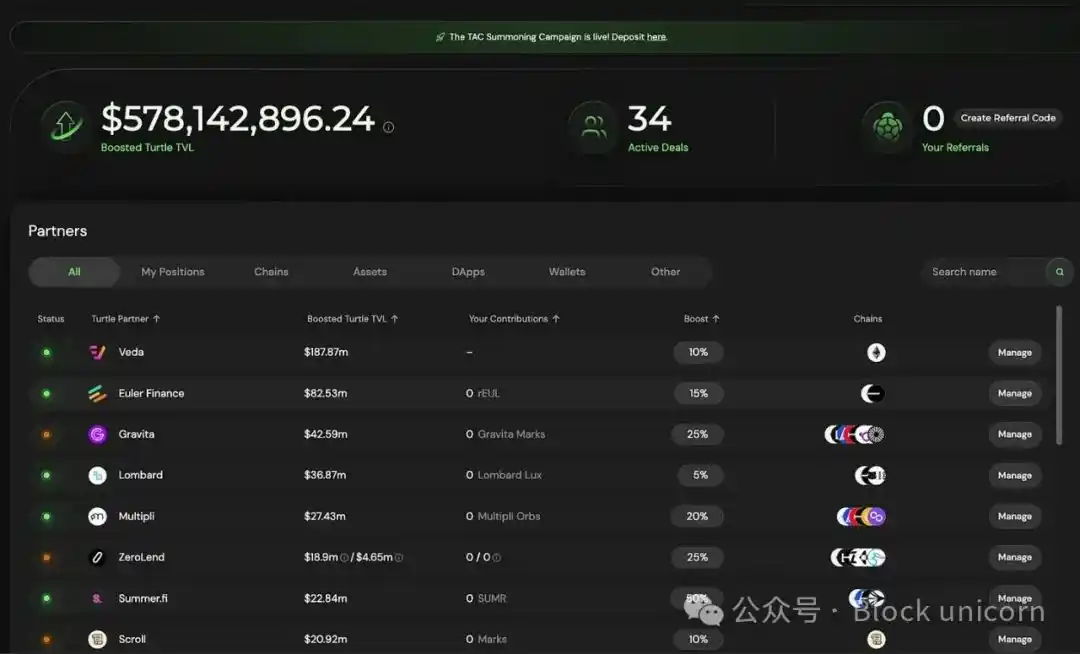

Today, protocols like turtleclubhouse and roycoprotocol are driving this liquidity: rather than blind issuance, they auction incentive mechanisms to liquidity providers (LPs) based on demand signals.

Essentially: "You bring the liquidity, we direct the incentives where they matter most." This unlocks a second-order effect: the protocol no longer needs to forcefully acquire liquidity but rather coordinate it.

Turtle Club

One of the lesser-known yet highly effective bribe markets. Their pools are typically embedded in partnerships, with a Total Value Locked (TVL) exceeding $5.8 billion, employing dual-token issuance, weighted bribes, and surprisingly sticky Liquidity Provider (LP) bases.

Their model emphasizes fair value redistribution, meaning issuance is guided by voting and real-time capital velocity metrics. This is a smarter flywheel: LPs are rewarded based on the effectiveness of their capital rather than just size. This time, efficiency is finally incentivized.

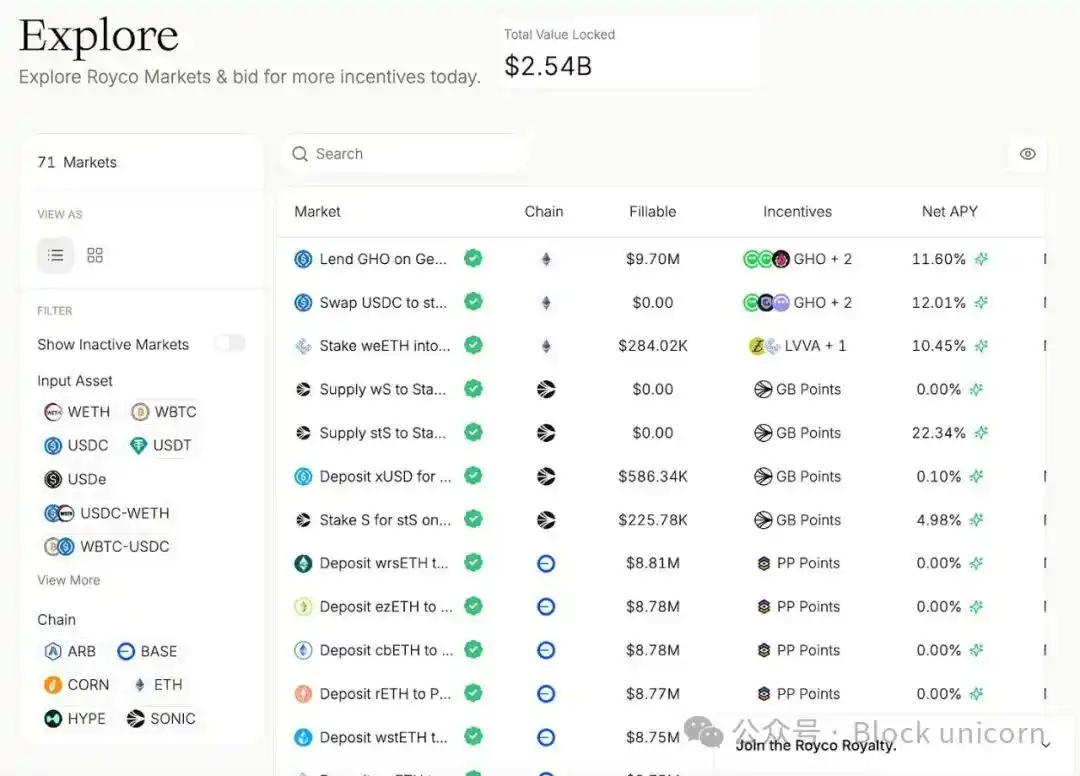

Royco

Within a month, its TVL surged to $26 billion, representing a month-over-month growth of 267,000%.

While some of it is "points-driven" capital, what's crucial is the infrastructure behind it:

· Royco is a liquidity preference book.

· Protocols cannot just offer rewards and hope. They make requests, and LPs decide to allocate funds, ultimately coordinating into a market.

This narrative is not just about the meaning of the yield game:

· These markets are becoming the meta-governance layer of DeFi.

· HiddenHandFi has accumulatively sent over $35 million in bribes across major protocols such as VelodromeFi and Balancer.

· Royco and Turtle Club are now shaping the effectiveness of issuance.

Mechanism of Liquidity Coordination Market

1. Bribery as a Market Signal

Projects like Turtle Club allow LPs to see where the incentives are flowing, make decisions based on real-time metrics, and earn rewards based on capital efficiency rather than just capital size.

2. Liquidity Request for Listing (RfL) as an Order Book

Projects like Royco enable protocols to list liquidity demands like orders on a market, with LPs filling them based on expected returns.

This becomes a two-way coordination game, rather than one-way bribery.

Ultimately, if you decide the direction of liquidity, you influence who can survive the next market cycle.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

[Initial listing] Bitget to list Cysic (CYS) in the Innovation zone

100% rebate for KYB users: Earn fee rebates on EUR bank deposits!

[Initial listing] Bitget to list Talus (US) in the Innovation and AI zone

Bitget Trading Club Championship (Phase 21)—Up to 1250 BGB per user, plus a ZETA pool and Mystery Boxes