Web3 Lawyer Analysis: How Can Mainland Companies Successfully Issue RWA Products in Hong Kong?

In this wave of financial innovation, Hong Kong has rapidly emerged as a pioneer in Regulatory and Compliance (RegTech) development in the field of Risk-Weighted Assets (RWA), leveraging its unique institutional advantages.

Original Article Title: "Web3 Lawyer In-Depth Analysis: How Mainland Enterprises Can Successfully Issue RWA Products in Hong Kong?"

Original Article Authors: Gui Ruofei, Sha Jun, CryptoSands Law Firm

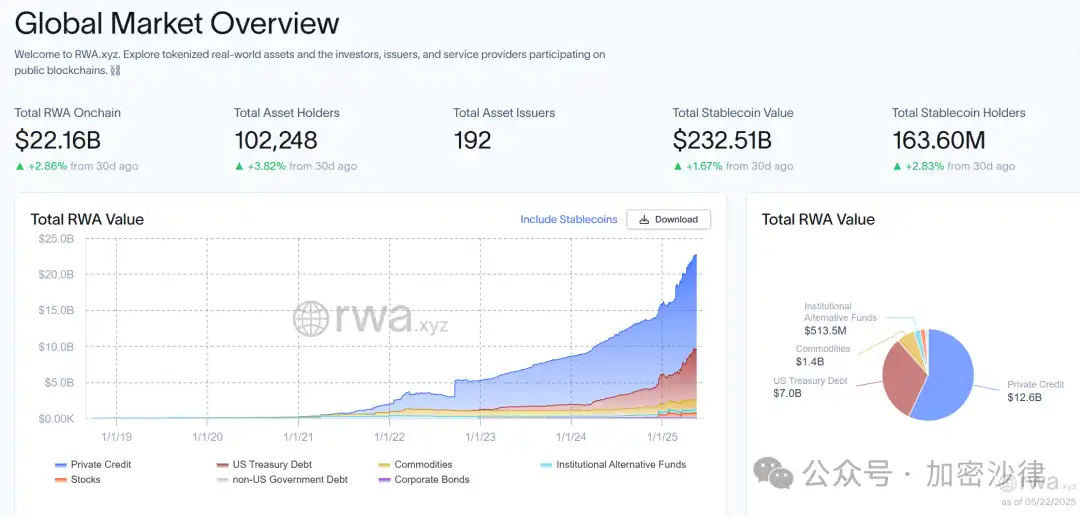

The global asset tokenization process is showing an accelerating trend. According to data from the RWA.xyz platform, as of April 2025, the total value of global on-chain RWA assets has exceeded $220 billion. At the same time, Deloitte also predicts in a research report that the size of the tokenized real estate market will reach $40 trillion by 2035.

In this wave of financial innovation, Hong Kong has rapidly developed into a leader in compliant RWA development due to its unique institutional advantages—from the charging pile asset tokenization project launched by the Langxin Group to the first compliant tokenized fund in Asia launched by Huaxia Fund. The successful implementation of multiple landmark cases has confirmed the potential application of this innovative financing method in the realm of real-world assets.

· What Exactly is RWA?

· Why Choose RWA, and What are Its Advantages?

· How Does Hong Kong Regulate RWA?

· What Compliance Key Points Should Mainland Enterprises Pay Attention to When Conducting RWA in Hong Kong?

The CryptoSands Law Firm team has been deeply involved in the cryptocurrency industry for many years and has rich experience in handling RWA project architecture design and related complex cross-border compliance issues. In this article, the team will combine their latest RWA project experience and industry research results to provide a professional lawyer's perspective to outline and answer the above questions.

(The above image is a global on-chain RWA assets dashboard compiled by the RWA.xyz website)

1. What Exactly is RWA?

RWA, the English acronym for "Real World Assets," refers to the tokenization (or "tokenization") of real-world assets, which is an innovative financial model based on blockchain technology. It uses blockchain technology to map physical assets or financial assets onto the chain, transforming them into highly liquid and divisible digital tokens. This transformation not only achieves digital representation of assets but also endows these real-world assets with unprecedented transparency and traceability through blockchain technology.

While we can expound on the connotation and extension of the RWA concept at a theoretical level, when it comes to the specific project implementation level, it is challenging for all parties to reach a complete consensus.

“What exactly is genuine RWA? Which projects should be identified as RWA projects?” — For the above questions, professionals, regulatory bodies, and project teams all have their own perspectives and viewpoints. The Crypto Salad team, combining project experience and research results, has provided their viewpoint from a legal compliance perspective: “RWA is actually a broad concept, and there is no so-called standard answer. All processes that achieve asset tokenization through blockchain technology can be called RWA.” For a detailed analysis of the RWA concept, see: “Web3 Lawyer Deciphers: What Type of RWA is Everyone Understanding?”

II. Why Choose RWA and What Are Its Advantages?

(A) Unlocking Heavy Asset Financing Scenarios Inaccessible to Traditional Finance

Firstly, taking assets such as real estate, infrastructure revenue rights, and commodities as examples, these types of assets are difficult to finance through traditional financial instruments due to their heavy asset nature, liquidity constraints, and complex issues such as compliance and regulation. The RWA model, combined with blockchain technology, divides the ownership of these physical assets or equity assets, transforming them into highly liquid digital tokens, and raises funds from investors through the issuance of digital tokens. RWA has opened up a new financing method for the aforementioned assets, allowing these originally “dormant” assets to be revitalized. This means that in the current environment of few financing channels, high financing difficulties, and high financing costs, RWA can provide an enterprise with a new “lifeline.”

For investors, the divisibility of tokens reduces the investment threshold for specific assets. Taking real estate investment as an example, under the traditional financial framework, investors looking to invest in real estate often need to spend millions of dollars to acquire full property rights. The high financial threshold excludes many small and medium investors. However, through the RWA model, investors may only need to spend $50 to acquire a token representing partial ownership of real estate. By holding this token, investors can enjoy the appreciation of the real estate and investment returns from rent.

(B) Reducing Financing Costs and Improving Financing Efficiency

In the traditional securities issuance process, enterprises and projects need to undergo a strict and lengthy approval process, and the qualifications, scale, and operational methods of the issuer must meet high requirements. Taking the issuance of asset-backed securities (ABS) as an example, its regulatory and approval standards are extremely strict, which greatly limits the financing needs of some enterprises.

Under the RWA model, in addition to complying with local regulatory requirements, the financing party has relatively fewer other admission requirements and restrictions, but still needs to ensure compliance with the underlying assets. Therefore, this financing method to some extent avoids the lengthy review process and cumbersome issuance procedures in traditional financing, effectively reducing the cost of financing.

(3) Customized Transaction Structure

RWA financing provides enterprises with unprecedented flexibility, allowing them to tailor financing structures to market demand and their own development goals. Enterprises can autonomously design key terms such as revenue distribution models, redemption mechanisms, token unlocking mechanisms, and adjust issuance conditions in real-time based on market dynamics. This high level of flexibility enables enterprises to precisely match investor expectations and risk preferences, thereby enhancing the targeting and success rate of financing.

Fundamentally, in addition to introducing blockchain technology to improve financing efficiency and transparency, RWA has also changed the financing logic under the traditional financial framework. Traditional financing models, whether debt financing or equity financing, mostly rely on corporate credit as the foundation. In contrast, RWA, leveraging blockchain technology, has achieved effective isolation between "corporate credit" and "asset credit". Therefore, even if the issuer's credit condition is average, as long as the underlying assets are of high quality, financing can be conducted based on the asset's own credit.

This characteristic is similar to the ABS model mentioned above. However, while the two have similarities in financing logic, the core difference between them lies in the investor base and the ecosystem effects they form. The ABS market is mainly led by traditional financial institutions, with a relatively limited participant base, and most transaction parties are institutional investors. This characteristic results in insufficient overall transaction depth in the ABS market, a relatively narrow market coverage, and a lack of widespread influence.

In contrast, the participants in the RWA market are more diverse. In addition to traditional financial institutions, the RWA financial market also attracts numerous crypto investors and industry ecosystem partners. Therefore, in the RWA market, from professional institutions to retail investors and partners, all can freely buy, sell, and use the token, becoming an integral part of the token's ecosystem.

A large and active ecosystem and community form around RWA tokens. The strong community cohesion and ecosystem stickiness generated will provide strong support for the long-term value growth of RWA tokens, thereby driving the healthy development of the market. The prosperity of the on-chain ecosystem can also benefit the off-chain business development of the project parties significantly, and greatly enhance the brand exposure of the project parties.

This on-chain/off-chain collaborative positive feedback development model is the true ingenuity of the RWA model compared to traditional financing methods, and is also something that the ABS model finds difficult to achieve. Currently, the market is still continuously cultivating and expanding the RWA investor base. Leading the pack in the current RWA track are various types of financial asset tokenization products. Due to the high compliance, standardization, and low data acquisition difficulty of financial assets, financial asset tokens have a unique advantage and demonstration effect in the RWA track.

The wave of financial asset tokenization began with low-risk underlying assets such as U.S. Treasury bonds, money market funds, and other products. A typical example is the BUIDL tokenized investment fund launched by the global top asset management group BlackRock. As of now, the total market value of BUIDL has reached $28.9 billion. In addition to low-risk financial assets, high-risk assets such as stocks, ETFs, and other financial assets have recently embarked on the fast lane of tokenization. On May 22nd and 23rd, the Kraken exchange platform and Ondo Finance respectively announced plans to promote the tokenization and on-chain trading of stocks, ETFs, and other financial assets.

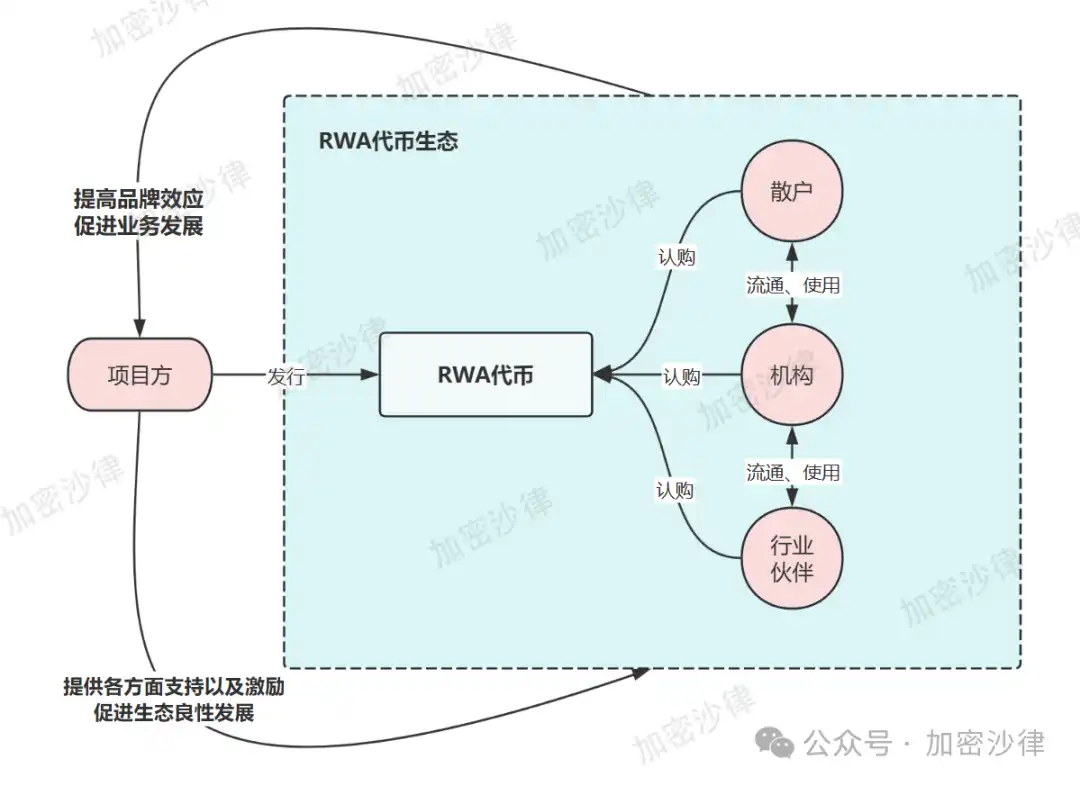

With the rapid implementation and development of various tokenized financial assets and stablecoins, the scale of investors and liquidity in the RWA market will reach new heights. In the future, an increasing variety of RWA products will enter the investor's field of vision, attracting more Web2 users and traditional financial investors to enter the RWA ecosystem. The flywheel of the entire RWA ecosystem will cycle rapidly, bringing new wealth effects and industry opportunities.

(The above diagram is an illustrative diagram of the RWA ecosystem development model, for reference only)

Three, How Does Hong Kong Regulate RWAs?

(I) Regulatory Principles

As a key force in market regulation in Hong Kong, the Securities and Futures Commission (SFC) has adopted a "See-Through Approach" in regulating RWA products. The core of this principle is that the regulatory focus is not on whether the product is in the form of a "token" but rather on the financial attributes of the real assets underlying the token. In short, Hong Kong's regulation of RWA aims to return to the essence of the underlying assets, rather than being confined to the form of tokens. This regulatory principle is also a concrete embodiment of the "same business, same risk, same rules" concept.

(II) Specific Regulatory Documents

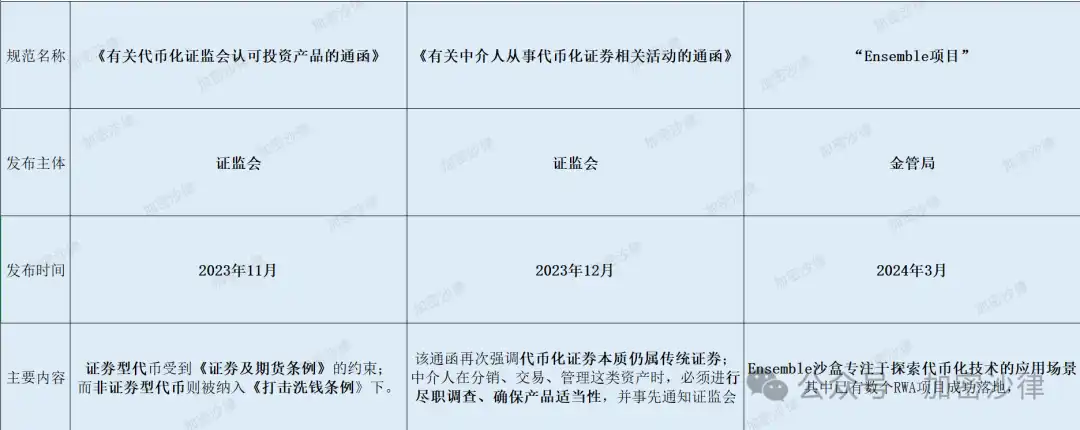

1. In November 2023, the Securities and Futures Commission (SFC) of Hong Kong issued a circular on "Regulatory Framework for Tokenized SFC-authorized Investment Products," which clearly outlines the tiered regulatory concept for securities token issuance. According to the relevant regulations, tokenized securities are governed by the Securities and Futures Ordinance and must meet the requirements set out in the circular, including token issuance qualifications, disclosure of information, and investor suitability. Non-securities tokens are included in the scope of regulation under the Anti-Money Laundering Ordinance.

2. In November 2023, the Securities and Futures Commission of Hong Kong issued the "Circular on Intermediaries Engaging in Activities Related to Tokenized Securities." The circular once again emphasized that while tokenized securities are issued using blockchain technology, they are fundamentally traditional securities and must comply with existing securities regulations. In addition, intermediaries must conduct due diligence when distributing, trading, or managing such assets, ensure product suitability, and notify the Securities and Futures Commission in advance.

3. In March 2024, the HKMA launched the "Ensemble Project." The Ensemble Sandbox focuses on exploring the application scenarios of tokenization technology, with several RWA projects already successfully implemented, covering various industries such as green bonds, carbon credits, real estate, and supply chain finance.

Overall, from 2023 to 2024, the Securities and Futures Commission of Hong Kong sequentially released multiple circulars and guidance documents relating to tokenized investment products, further clarifying the specific regulatory standards for RWA products (especially tokenized securities). This provided clear regulatory guidance for the sound development of the RWA market.

(The above diagram summarizes the RWA-related regulatory framework)

The above analysis specifically interprets Hong Kong's regulatory framework for RWA, while a comprehensive and systematic review of Hong Kong's virtual asset regulatory policies can be found in the following article: "A Comprehensive Guide: Systematic Review of Hong Kong's Virtual Asset Regulatory Framework."

4. What Compliance Key Points Should Mainland Chinese Companies Note When Conducting RWA in Hong Kong?

The reason why the issuance of RWA must adopt a cross-border architecture is that in mainland China, token issuance is a regulatory red line that cannot be crossed. On September 4, 2017, the People's Bank of China and seven other departments issued the "Notice on Preventing the Risks of Token Issuance Financing," clearly stating that any organization or individual shall not engage in illegal token issuance financing activities, and all types of token issuance financing activities shall cease immediately.

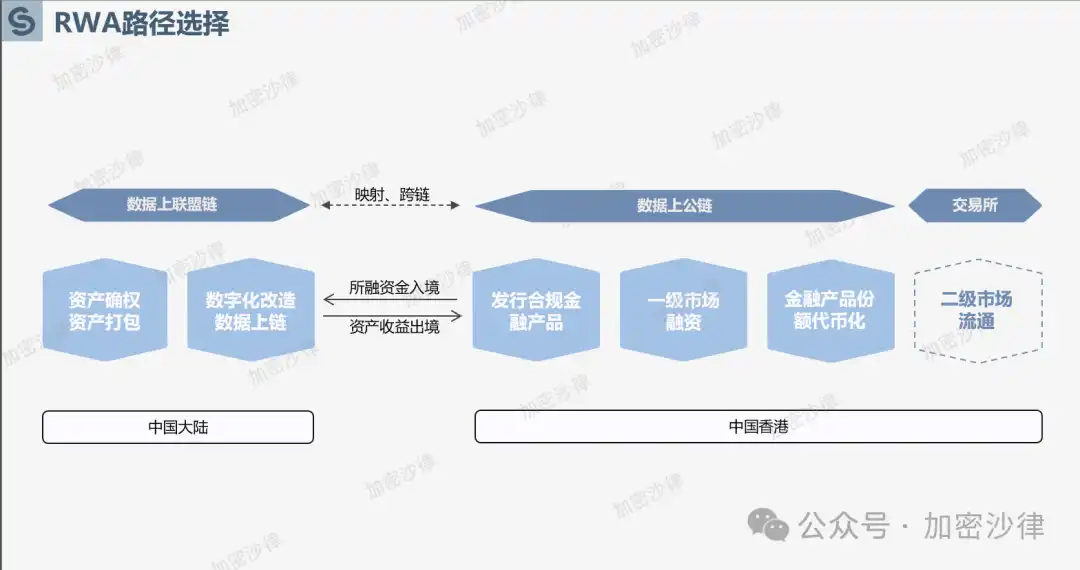

Therefore, the coin issuance behavior of RWA projects in mainland China must occur overseas. Hong Kong, due to its sound regulatory framework, friendly policy attitude, and rich industry ecosystem, has become one of the best choices for Chinese enterprise RWA projects to land. The following sections will analyze the key compliance points and framework design ideas for conducting RWA projects in Hong Kong from the perspectives of underlying assets, data on-chain, and fund circulation.

(The above diagram is an illustrative overview of the overall framework for issuing RWA in Hong Kong)

(1)Underlying Asset Compliance

1. Asset Ownership

Since the essence of RWA is the tokenization of real-world assets, the token holders will directly or indirectly have specific ownership rights to real-world assets. Therefore, to ensure the subsequent issuance, transfer, and redemption of RWA tokens can be conducted legally, the underlying asset owner, i.e., the RWA project party, must ensure clear and legal ownership of the asset. The RWA project compliance team needs to conduct a detailed due diligence on the underlying assets during the project implementation to ensure ownership legitimacy. Specifically, the compliance team will conduct ownership dispute resolution, collect and verify ownership proof documents, public registration information, litigation status, collateral, mortgage, or judicial freeze status of the underlying asset during the due diligence process.

2. Asset Audit

After completing asset ownership confirmation, the project party also needs to engage a professional auditing firm to audit the underlying assets. The audit report will provide reference data for the subsequent asset pricing and issuance, including but not limited to the following elements:

· Asset Market Value - Conduct a fair market value assessment by professional appraisers or valuation experts, referencing historical transaction data, market trends, and similar asset prices.

· Asset Depreciation and Impairment - For fixed assets, consider depreciation methods, asset useful life, and possible impairment situations to ensure the assessed value reasonably reflects the actual value.

· Asset Risk Identification - Identify risks associated with the asset, such as market risk, legal risk, liquidity risk, operational risk, etc.

3. Asset Segregation

As mentioned earlier, the core value of RWA lies in financing directly based on high-quality asset credit, thus moving away from the traditional financing model based on corporate credit. Therefore, when conducting an RWA project, it is necessary to segregate the underlying asset from the actual operating entity of the project party to achieve risk isolation between the operating entity and the underlying asset. The following practical example from the Crypto Salad team's ongoing initiative will illustrate one of the asset segregation architectural designs:

· Firstly, the project compliance team will assist the project party in establishing an SPV (Special Purpose Vehicle) domestically.

· Secondly, the actual operating entity will transfer the underlying asset to the SPV through a buy-sell transaction.

· Finally, the SPV will enter into an operations services agreement with the project party, where the project party is responsible for operating and managing the underlying asset, and the SPV will periodically pay the project party the corresponding service fees.

(The above diagram is a schematic design of the asset securitization framework, for reference only)

In conclusion, through this asset securitization framework, the project party can transfer asset ownership to an SPV company, achieving risk isolation while facilitating subsequent asset packaging and issuance. Meanwhile, although the actual operating entity no longer owns the asset, they can continue to manage and operate the underlying asset through a service agreement.

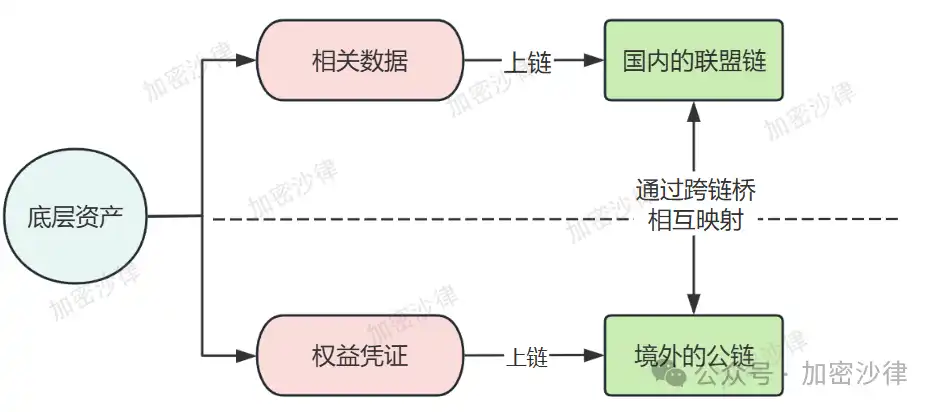

(II) On-chain Data Compliance

Due to the strict regulations in China regarding cross-border data transmission and data exchange, most RWA projects choose not to transfer related data overseas and circulate and disclose it on a public chain. During the research process, the Encrypted Salad team found that, while meeting the compliance requirements of China's Data Security Law and Personal Information Protection Law, project parties are more inclined to choose the "two-chain-one-bridge" model to achieve on-chain data.

Specifically, RWA asset data is selected to be put on-chain on a domestic consortium chain for notarization, while the corresponding RWA token is deployed on a high-performance public chain overseas. The RWA token circulating overseas and the on-chain data in China are mapped and bound through a cross-chain bridge. This architectural design not only solves the on-chain notarization issue of RWA underlying asset data, ensuring the transparency and traceability of asset data, but also avoids the compliance red line of cross-border data transmission.

(The above diagram is a schematic of the "two-chain-one-bridge" model, for reference only)

In addition to the "two-chain-one-bridge" model, RWA projects can also rely on the Hainan Free Trade Port Cross-Border Data Flow Test Zone (hereinafter referred to as the "Hainan Data Port") to achieve cross-border data on-chain and circulation. According to the disclosed information, the Encrypted Salad team has summarized the core framework of the current Hainan Data Port data exit plan as follows:

1. The regulatory agency actively classifies and grades the data;

2. Establish a data whitelist, where data included in the whitelist can directly exit without approval;

3. If the data is not on the whitelist, the regulatory agency will apply corresponding regulatory procedures based on different data types: personal information protection certification, data export security assessment, personal information export standard contract filing, etc.

During the actual project implementation process, the Encrypted Salad team found that, in addition to the compliance requirements in the data circulation process, there are also key compliance points and administrative regulatory requirements in the data collection, storage, de-identification, packaging, and other stages of RWA underlying assets. Due to the length of this article, these points are not discussed here.

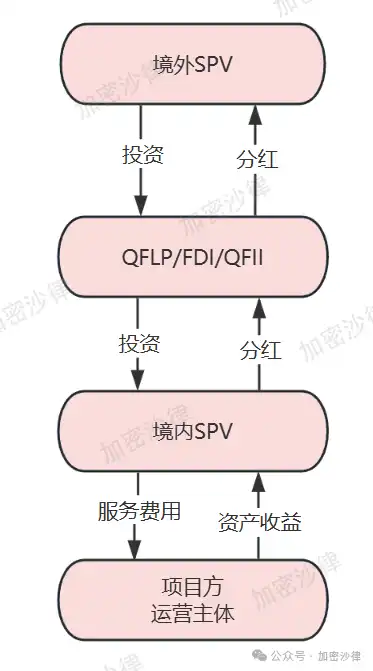

(3)Funds Circulation Compliance

Due to the strict foreign exchange controls in China, funds raised through the issuance of RWA overseas cannot be directly transferred to domestic operating entities. Therefore, a compliance team needs to design a specific framework and path for the overseas fund collection and circulation. Based on the project experience of the Cryptocurrency Salad team, after an RWA project raises funds through token issuance overseas, the funds held by the overseas SPV are generally collected through a fund channel and eventually transferred to the actual operating entity. There are three options for the fund channel in this architecture:

1. QFLP (Qualified Foreign Limited Partner)

2. FDI (Foreign Direct Investment)

3. QFII (Qualified Foreign Institutional Investor)

When designing the fund circulation architecture, the compliance team generally needs to consider the following factors: tax burden, access threshold, procedural requirements, compliance costs, etc. During the actual project implementation process, the project team must also pay attention to compliance. The preparation of declaration materials for different fund channel entities, feedback from authorities, and adjustments and improvements to the corresponding frameworks all require full support from a professional legal team.

(The above image is a schematic diagram of the RWA project's funds circulation channel for reference only)

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CandyBomb x ZBT: Trade futures to share 100,000 ZBT!

Bitget Builder+ Initiative is now recruiting!

Bitget releases September 2025 Protection Fund Valuation Report

[Initial Listing] Bitget Will List Revive (RVV) in the Innovation Zone