From Bearish to 25x Oversubscribed, the Great Reversal of Circle's IPO

2 months ago, the valuation was halved amid acquisition rumors, and 2 months later, everyone is FOMO-ing in the midst of a funding frenzy.

One month ago, the most discussed topic about stablecoin issuer Circle on social media was still the rumor of "selling $4 billion to Coinbase or XRP." After Circle released its prospectus in early April, industry doubts about its declining market share, low gross margin, and single revenue channel were constant. Industry insiders generally believe that Circle's IPO plan, restarted after many years, may be challenging to impress the market.

However, the enthusiasm for the stablecoin concept has completely exceeded the expectations of crypto practitioners: Circle went public at $31 per share, reaching a valuation of $6.9 billion, with an oversubscription ratio as high as 25 times, becoming the most anticipated IPO in the crypto industry in recent years. What caused such a dramatic reversal in market sentiment? Has Circle's fundamentals truly improved, or is the market undergoing an "emotional reevaluation" of the stablecoin narrative?

Two Months, Market Expectations Dramatically Reversed

Around April of this year, when stablecoin issuer Circle reinitiated its IPO plan, the market's attitude was generally cautious, if not bearish. Many analyses pointed out structural bottlenecks in Circle's business, such as excessive reliance on USDC reserve interest, low gross margin, and insufficient revenue growth momentum.

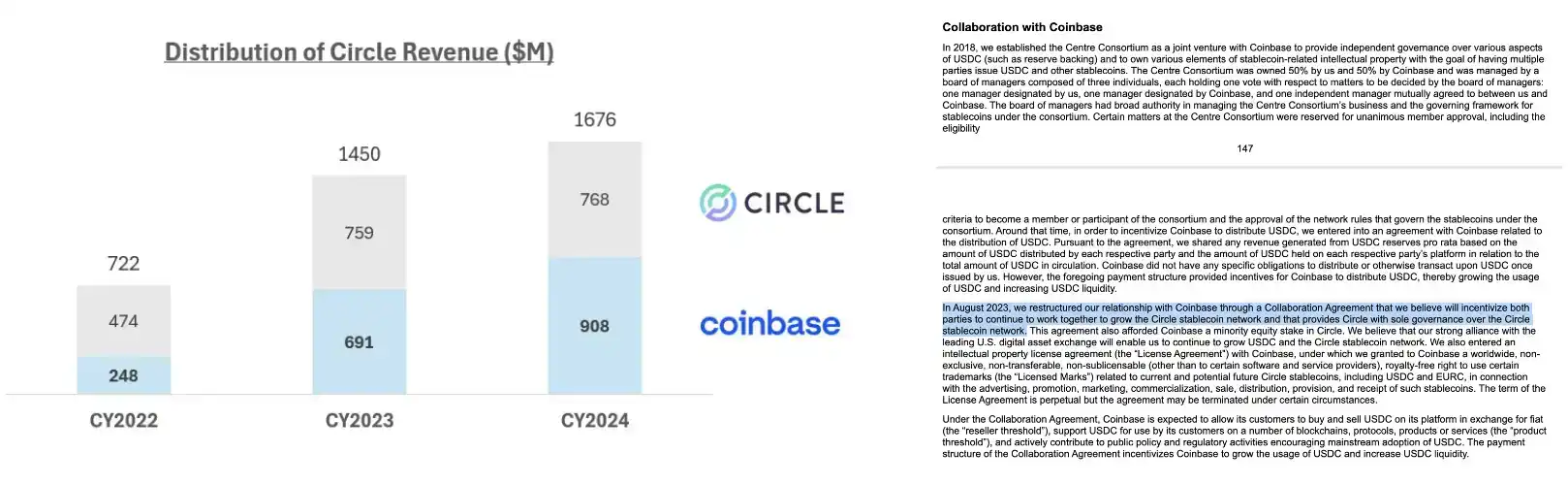

According to Circle's prospectus, its revenue for the 2024 fiscal year is around $1.67 billion, a 16% year-on-year growth, but net profit plummeted from $267.6 million in 2023 to $155.7 million in 2024, a 41.8% decrease. On one hand, the interest income from USDC is a pro-cyclical dividend, and once the Fed enters a rate-cutting cycle, Circle's reserve income will systematically decline. On the other hand, Circle has incurred high costs to promote USDC, especially a 50% distribution cost paid to Coinbase, resulting in an extremely low gross margin. Statistics show that Circle's gross margin has plummeted rapidly from 62.8% in 2022 to 39.7% in 2024.

Detailed description of Coinbase revenue-sharing terms in Circle's prospectus

In short, many investors question: Circle's profit model is too single and fragile, lacking long-term prospects.

At the same time, rumors of Circle's sale were circulating in the market. In May, Cointelegraph reported that crypto giants including Ripple and Coinbase had considered acquiring all of Circle at a valuation price of 40 to 50 billion dollars, and the deal even came close to completion. Although Ripple's CEO later personally denied the acquisition rumor, stating "never sought to acquire Circle," and Circle emphasized that "the company is not for sale," the mere appearance of the rumor itself indicates the industry's lack of confidence in Circle's prospects—when a company is rumored to be willing to sell itself at a price equivalent to or far below its previous SPAC valuation (sought a $9 billion listing in 2022), it inevitably raises questions about its independent development capabilities.

In addition, the decreasing market share of USDC is also a fact. Since the Silicon Valley bank scandal in 2023, the circulation of USDC has drastically shrunk from its peak, with market share being squeezed by competitor USDT. These factors combined made Circle two months ago seem unattractive, with many holding a reserved or even bearish view on its IPO prospects, believing that fundraising may face a cold reception.

However, just two months later, the market sentiment has made a 180-degree turnaround. Circle officially started its IPO pricing in early June, with enthusiastic investor subscriptions. Not only did the issuance size increase from 24 million shares to over 34 million shares, but the issuance price was also raised from the original $24 per share to $27 per share, bringing its overall valuation back up to $6.2 billion. In the end, Circle completed the issuance at $31 per share, receiving over 25 times oversubscription and raising approximately $1.1 billion.

This fervent subscription situation has dispelled the previous low expectations in the market. More notably, this IPO attracted the eager participation of top institutions: the underwriting lineup was led by Wall Street investment banks such as JPMorgan Chase, Citi, and Goldman Sachs, with BlackRock subscribing to about 10% of the shares, and Ark Investment Management subscribing to $150 million. Driven by strong demand, there was a shift in Circle's initial plan for a large-scale exit by early shareholders: the secondary sale initially arranged in the prospectus accounted for as much as 60% (14.4 million shares, sold by founders and VCs), but it was reduced to 8 million shares, representing only 25%. This adjustment means even Circle's internal shareholders chose to sell less and hold more, illustrating the high market enthusiasm.

Behind the Sentiment Reversal, Has the Fundamentals Changed?

Over the past two months, the stablecoin sector has successively received heavyweight regulatory good news, creating an excellent policy environment for the Circle IPO.

In late May, the U.S. House Financial Services Committee overwhelmingly passed the so-called "GENIUS Act," a stablecoin regulation bill. This bill aims to establish a clear federal regulatory framework for dollar-pegged stablecoins, indicating that stablecoin issuers are likely to bid farewell to the gray area and enter a licensed and compliant new stage.

For Circle, this is a massive policy boon—once stablecoin status gains legal recognition, the market will reevaluate the compliance and sustainability of its business model. Circle astutely chose to go public during this window, seen in the industry as a combined "regulatory arbitrage + market reassessment" bonus, meaning they preemptively completed compliance endorsement on the eve of the bill's formal landing and gained investor and policymaker approval through a U.S. stock market listing.

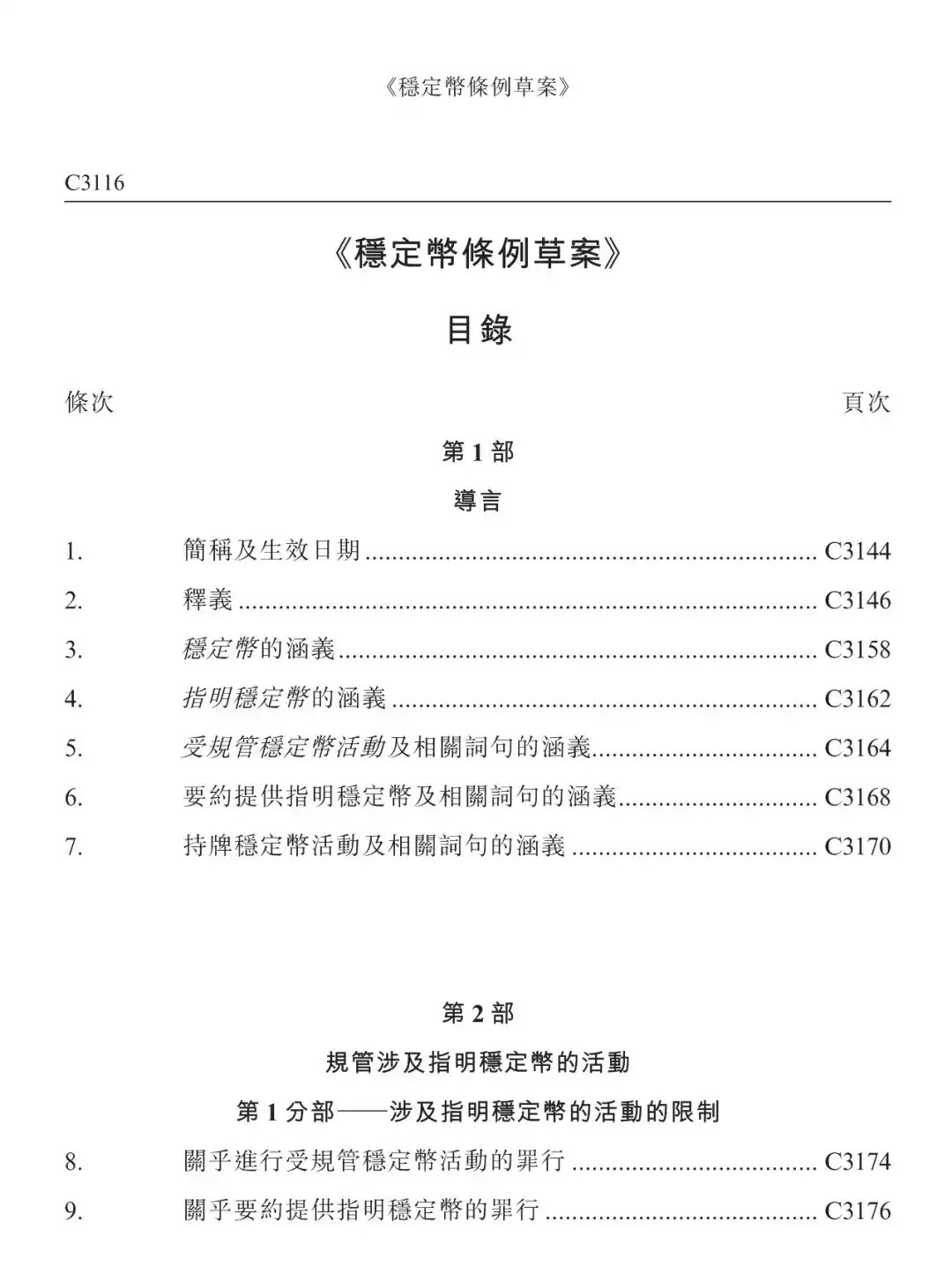

In addition to the United States, Hong Kong, China also rolled out a stablecoin regulatory framework during the same period. On May 30, the Hong Kong SAR Government published the "Stablecoin Ordinance" in the Gazette, marking the official enactment of the ordinance. Previously, on May 21, the Hong Kong Legislative Council passed the final reading of the draft ordinance, establishing a licensing regime for stablecoin issuers pegged to fiat currency. This means that Hong Kong will become one of the few jurisdictions globally, apart from the United States and the European Union, with clear stablecoin regulatory rules.

Table of Contents of the Hong Kong Stablecoin Ordinance Draft, which was approved by the Hong Kong Legislative Council on May 21

This series of new changes in the global regulatory environment has significantly boosted market confidence in the prospects of compliant stablecoins, setting the tone for Circle's valuation reassessment.

The second key driver behind the shift in market sentiment comes from strong "buy-in" by heavyweight institutional investors. At the end of May, Ark Investment Management, under Cathie Wood, expressed interest in purchasing up to $150 million in Circle IPO shares. In addition, the global asset management giant BlackRock plans to subscribe to approximately 10% of the issued shares, with both institutions collectively subscribing for about 30% of this financing round.

BlackRock's participation is particularly significant for Circle. On the one hand, BlackRock began deep cooperation with Circle as early as 2022, with Circle agreeing to have at least 90% of the USDC reserves managed by BlackRock. In exchange, BlackRock pledged not to issue its stablecoin for four years. This agreement not only enhances the security and liquidity management of USDC reserves but also provides Circle with the endorsement of a traditional financial giant.

Behind the phenomenon of Wall Street's "major buy-in" subscription is a high-stakes bet on compliant stablecoins and a reevaluation of Circle's global expansion capabilities and USDC's dominant position in the ecosystem. Many Wall Street institutional investors have previously shied away from pure crypto businesses but can now indirectly invest in the expected expansion of the cryptocurrency market through Circle. The recognition of major institutions has also significantly influenced the market's attitude towards Circle.

However, regulatory legislation and institutional entry undoubtedly follow long-term logic: they validate the stablecoin industry, open up future growth space, and are not mere speculative hype. Yet, in the medium to short term, the rebound in USDC market cap and the frenzy of subscriptions have some pro-cyclical emotional factors. Since the second quarter of this year, with the surge in Bitcoin prices and the overall warming of the crypto market, the stablecoin sector has taken advantage of the situation by constantly creating hype, and the frenzy of the Circle IPO subscription seems more like a short-term excess demand driven by investor FOMO.

Currently, the United States is still in a high-interest-rate environment, and Circle enjoys a significant interest income. Many institutions, including Circle itself, hope to take advantage of this performance boost before the interest rate cut arrives, to some extent playing a game of short-term performance. Once the Federal Reserve begins to lower interest rates, the market may reassess Circle's profitability. If Circle's fundamentals are disproved in the future (for example, if USDC growth does not meet expectations or gross margin fails to improve), the current optimism may also fade.

In many traditional media commentaries, the stablecoin's triple attributes of "policy endorsement, technological imagination, and industry implementation" align with the market's preference for themes that are "storytelling, implementable, and policy-supported." However, for Circle, behind the hype of the theme, its ability to deliver still needs time to be tested.

A $7 Billion Valuation, High or Low?

The IPO pricing of Circle corresponds to a valuation of about $6.9 billion. As the "first stock of stablecoin," the market does not seem to have established a consensus valuation model for it yet. So, is Circle's nearly $7 billion valuation reasonable?

In 2008, Visa completed its initial public offering with a financing amount of $17.9 billion, surpassing AT&T's $10.6 billion to become the largest IPO in U.S. history at the time. Circle aims to "replace the Visa payment system." The company's net profit in 2024 is $156 million. Based on a $7 billion valuation, the static P/E ratio is about 45 times. In comparison, Visa's 2024 fiscal year net profit is about $17 billion, with a market value of nearly $500 billion and a P/E ratio of around 30 times.

In terms of the profit model, Visa relies mainly on card processing fees, uses its market dominance as a moat, and has a steadily growing income and very high profit margins (gross margin consistently above 70%). In contrast, Circle has faced growth challenges in recent years (USDC's market share has been consistently suppressed by USDT, failing to effectively break through the 30% mark) and margin issues (maintained at around 30% in recent years), which have always been questioned by the industry. In terms of profit quality, Visa's profits come from diverse and stable sources, while Circle's profits mainly come from reserve interest, which is easily influenced by macro interest rate policies and cryptocurrency market cycles, resulting in greater volatility.

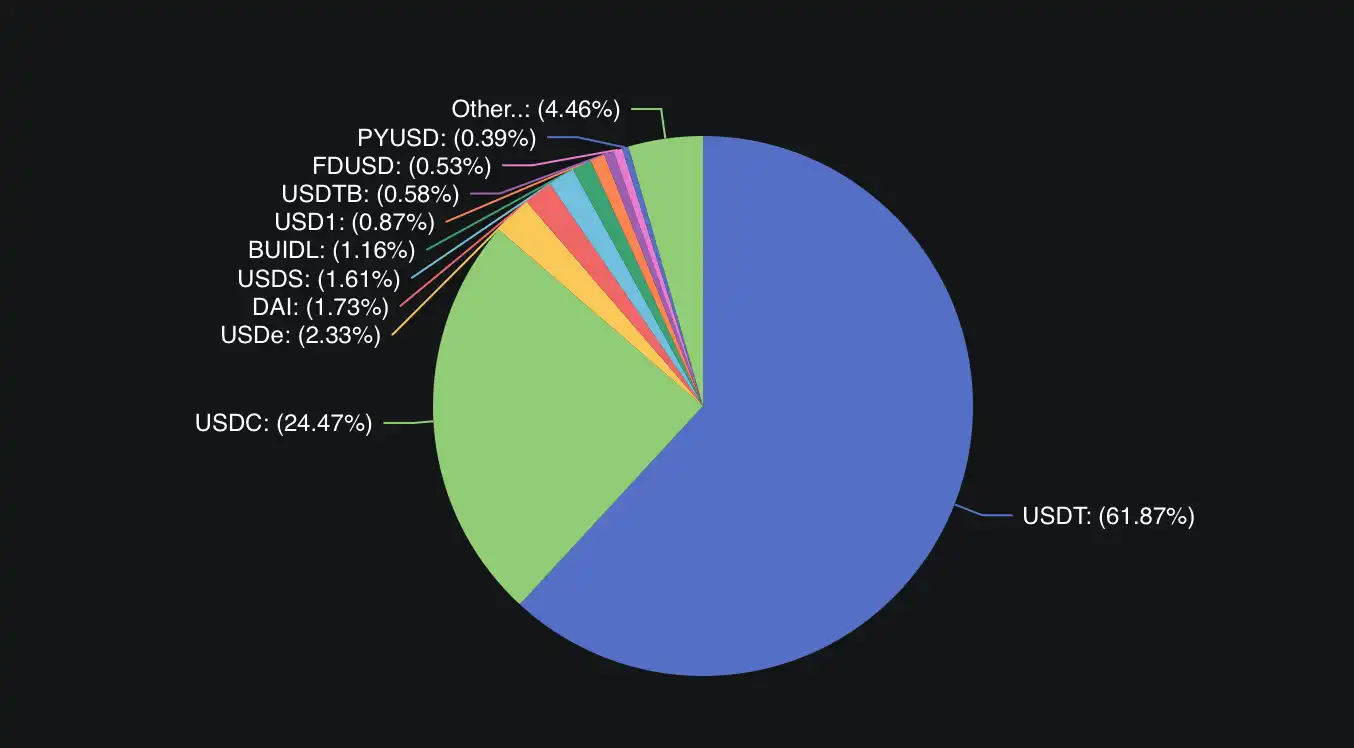

Stablecoin Market Share, Data Source: DeFiLlama

When it comes to replacing Visa, perhaps Tether and its USDT have more hope. By 2024, Tether achieved a super high profit of 14 billion dollars with 150 employees, with each person creating an average value of up to 93 million dollars, leaving Wall Street giants speechless. Simply estimating Tether's valuation at around 200 billion dollars based on a traditional financial company's 15x price-to-earnings ratio.

Some competitors outside the industry with publicly priced counterparts can also serve as a reference dimension. For example, the decentralized synthetic dollar protocol Ethena, whose stablecoin USDe issuance and business model are starkly different from Circle, does not rely on fiat currency reserves but is hedged by asset positions such as crypto derivatives and collateral to back the "synthetic dollar." Therefore, its revenue-generating ability is directly linked to the investment enthusiasm of the cryptocurrency secondary market. Earlier this year, Ethena's governance token ENA market cap briefly approached 40 billion dollars and has since stabilized at around 20 billion dollars over the past few months.

The market's high valuation multiples for Circle mainly stem from growth expectations. As a payment giant, Visa's mature enterprise grows slowly, while Circle operates in the stablecoin space in its early stages of rapid development. Investors may believe that under the "regulatory moat," the competition between Circle and Tether will face more variables, opening up more room for future profit growth.

On the other hand, whether Circle's valuation will inherit the volatility of the crypto market is also a major focus that the market needs to pay attention to and validate. The valuation fluctuation of the "first cryptocurrency stock," Coinbase, is a good illustration of this issue.

When Coinbase went public in 2021, its market cap briefly surged to 86 billion dollars, then the crypto market gradually turned bearish, and Coinbase's stock price underwent a significant correction, nearly approaching the hundred billion dollar mark. This volatility was once again evident in the first quarter of 2025, as Coinbase's stock price showed a high correlation with the cryptocurrency market, which is mainly focused on meme coins.

$COIN Price Trend, Coinbase's listing is widely regarded as a key marker of the 2021 crypto market transitioning from bull to bear; Data Source: Trading View

In comparison, Circle's 7 billion dollar valuation is just a fraction of Coinbase's. This reflects the difference in their business models and investor expectations: Coinbase, as an exchange, relies heavily on crypto trading volume for revenue, leading to performance fluctuations with market conditions; whereas Circle, as a stablecoin issuer, derives most of its revenue from reserve interest and related service fees, and investors believe that its valuation is less affected by the crypto market and more influenced by the macro interest rate environment.

It is worth noting that Coinbase currently also earns significant interest income through USDC reserve sharing (50%), and this part of the business is directly related to Circle. To some extent, Coinbase's valuation also includes a premium for its USDC business.

However, regardless, compared to Coinbase's initial public offering at a 300x price-to-earnings ratio, Circle's current valuation at around 45x appears much more moderate. The market seems to be valuing Circle based on the logic of a conventional financial services company rather than a tech unicorn. The view that the valuation of $7 billion leaves room for conservative estimates has become a mainstream opinion.

Asia Taking the Lead in Warming Up the Market?

While the Circle IPO is hot, the Asian capital market has already sparked a wave of enthusiasm for the "stablecoin concept." Concept stocks in the Hong Kong and A-share markets have recently experienced surging trends, with multiple stocks hitting consecutive daily limits or experiencing significant rallies, making stablecoins the new darling of the capital market seemingly overnight.

The reason for this is that the stablecoin concept has appeared for the first time in the Asian stock market. The stock market has previously speculated on concepts such as "blockchain," "web3.0," and "NFTs" from the crypto world, but the stablecoin concept has never appeared. In other words, the stablecoin concept is a completely new concept for most non-crypto people.

Additionally, with favorable policies, following the news of the Hong Kong "Stablecoin Regulation" at the end of May, the Hong Kong stock market took the lead in hyping the stablecoin concept. In early June, with Circle confirming its listing date, the Hong Kong and A-share sectors saw a coordinated surge, and within two days from June 2nd to 3rd, more than ten stablecoin-themed stocks in Hong Kong and A-shares collectively soared, showing astonishing gains. It is said that more than 20 brokerage firms issued over 30 stablecoin research reports overnight, keeping up with current events and telling everyone what this narrative is all about.

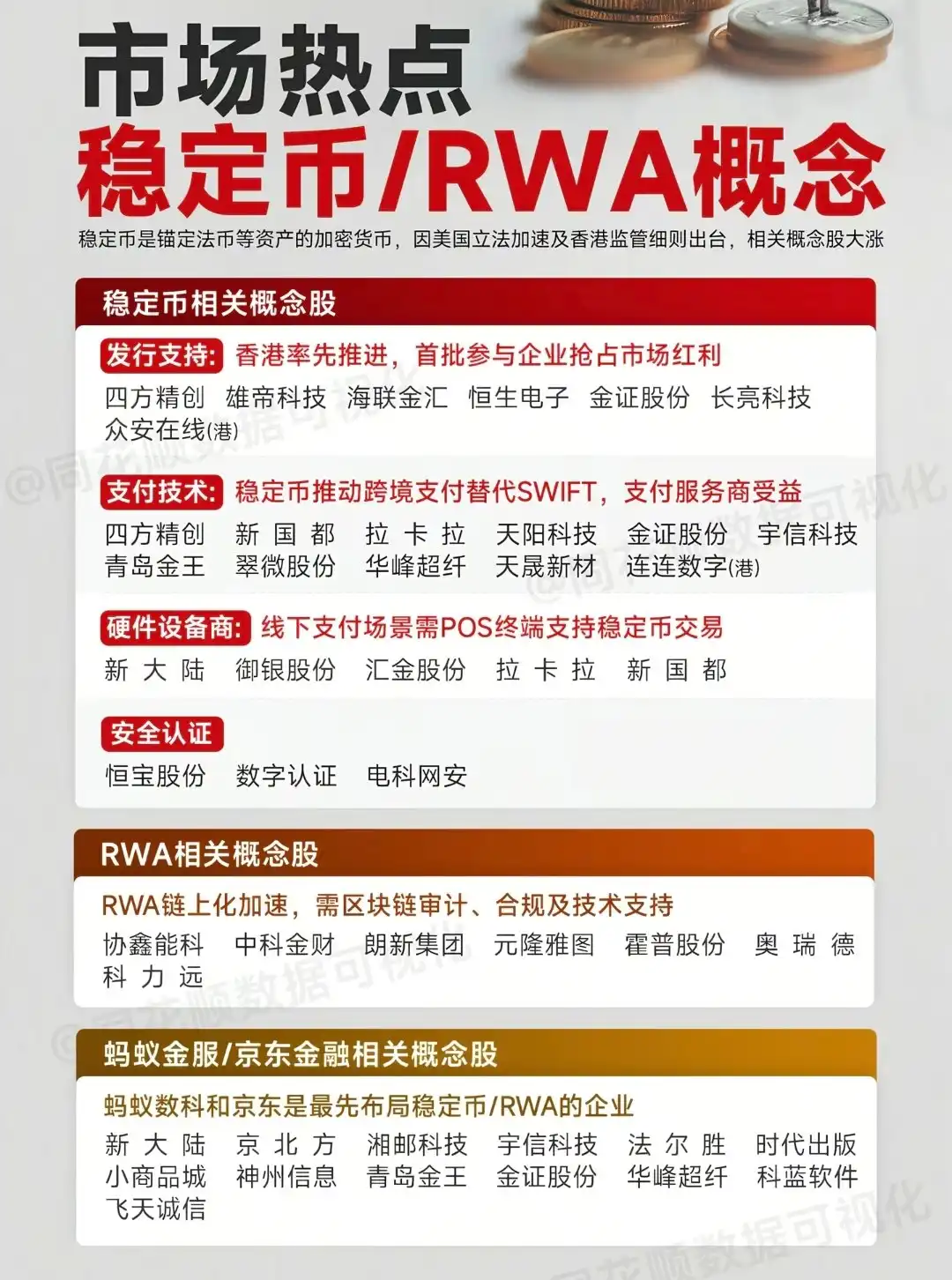

The most prominent stablecoin-related concept stocks currently in the Hong Kong and A-share markets are mainly divided into two categories: direct participation and indirect beneficiaries.

Direct participation targets are mainly concentrated in the Hong Kong stock market. These companies have direct equity or business relationships with stablecoin projects, making the benefit logic clear. For example, China Everbright Holdings (00165.HK) made a strategic investment in Circle in 2016, and the recent IPO will significantly increase Everbright's equity value, causing its stock price to surge, rising more than 26% at one point in the day. There is also Zhongan Online (6060.HK), whose investee company is involved in stablecoin issuance, and its bank provides stablecoin custody services, attracting hot money.

Indirect beneficiary targets are more common in the A-share market. These companies do not have direct stablecoin business, but their products/technologies can be applied to the stablecoin concept-related industry chain, making the logic more of a "possibility." For example, Cuiwei Share (603123), a company mainly engaged in general merchandise retailing, has developed a digital RMB payment scenario, being perceived by the market as the "pioneer of future stablecoin offline applications," leading to consecutive daily limit-up movements in its stock price; YuYin Share (002177) is an ATM and bank equipment manufacturer, as it has recently laid out digital currency ATMs, its stock has hit the daily limit for four consecutive days; companies like Sifang Creative (300468) and Xiongdi Technology (300546) have also been hyped by retail investors because they have been involved in digital payments, electronic identity recognition, and other businesses.

Market's Clarification of the Concept of Stablecoin-Related Underlying Assets, Image Source from Tonghuashun

As the first stock of a compliant stablecoin, its IPO has a greater significance in confidence transmission and trend confirmation—conveying the confidence in the mainstream recognition of stablecoins and confirming the trend of regulatory compliance and capitalization of stablecoins. In Hong Kong, the global attention brought by Circle's listing may indeed help the local stablecoin field to gain more endorsements and cooperation opportunities, attracting overseas funds to invest in Hong Kong's digital financial sector.

From widespread bearish sentiment two months ago to oversubscription by 25 times today, Circle has experienced a major market expectation reversal. As a bridge connecting the traditional financial and crypto worlds, stablecoins are receiving unprecedented attention and reassessment. Perhaps Circle's story is just the beginning, and with the implementation of the U.S. GENIUS Act and the issuance of a stablecoin license in Hong Kong, we may see a more mature and rational stablecoin ecosystem. By then, the market will speak through fundamentals to test whether the initial logic shift truly holds up.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

New spot margin trading pair — TREE/USDT!

Bitget to decouple loan interest rates from futures funding rates for select coins in spot margin trading

Bitget to decouple loan interest rates from futures funding rates for select coins in spot margin trading

ETH 10th anniversary—Bitget community carnival